Why People Buy Things They Cannot Afford

One of the most puzzling behaviors in personal finance is the tendency for people to purchase things they cannot truly afford. Expensive vehicles, luxury homes, premium electronics, designer products, lavish vacations, and lifestyle upgrades are often acquired despite limited savings, significant debt, and financial uncertainty. This behavior is so common that it has become a defining characteristic of many modern economies.

At first glance, this appears irrational. If a purchase creates financial stress, increases debt, or weakens long-term financial security, why would intelligent individuals willingly make such decisions? The answer lies in understanding the psychology behind spending. Most purchasing decisions are influenced by emotions, perceptions, social pressures, and cognitive biases rather than purely logical financial analysis.

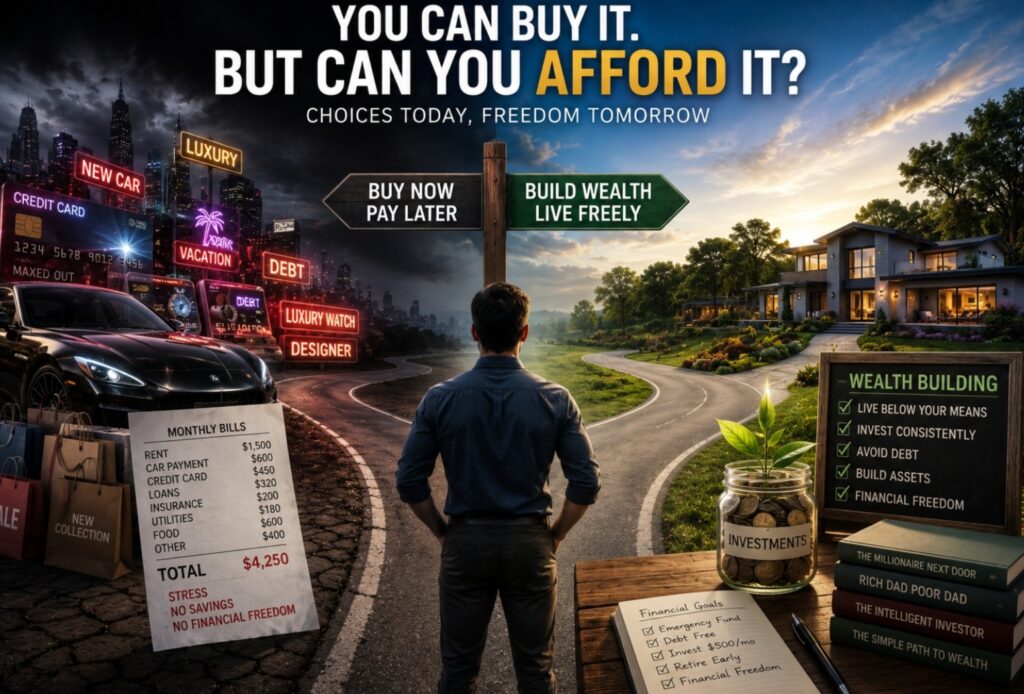

From an accounting perspective, affordability is not determined by whether a purchase can be obtained. Affordability is determined by whether a purchase can be sustained without damaging financial health. This distinction is critical because many consumers confuse access with affordability. Modern financial systems make it easier than ever to obtain products immediately, even when the long-term financial consequences may be harmful.

The question of why people buy things they cannot afford extends far beyond individual purchases.

It touches on deeper issues involving:

- Human psychology.

- Consumer culture.

- Social comparison.

- Identity formation.

- Emotional decision-making.

- Financial literacy.

- Behavioral economics.

Many people assume financial difficulties result primarily from insufficient income.

While income certainly matters, spending behavior often plays an equally important role.

Some individuals earning modest incomes build substantial wealth through disciplined financial habits.

Others earn impressive salaries yet remain trapped in debt because spending continually exceeds sustainable levels.

Understanding why people buy things they cannot afford is therefore not simply about consumer behavior.

It is about understanding one of the most powerful forces shaping financial outcomes.

The answers reveal important lessons about money, decision-making, and the psychology of wealth.

The Affordability Illusion

One of the most dangerous concepts in personal finance is the affordability illusion.

The affordability illusion occurs when people believe they can afford something simply because they can obtain it.

In reality, obtaining and affording are not the same thing.

For example:

- A bank may approve a large mortgage.

- A dealership may approve vehicle financing.

- A credit card may provide purchasing power.

- A lender may offer personal loans.

These approvals create access.

They do not automatically create affordability.

Affordability involves a broader financial assessment.

A purchase is truly affordable only when it can be sustained comfortably while maintaining:

- Healthy savings.

- Investment contributions.

- Emergency reserves.

- Reasonable cash flow.

- Long-term financial goals.

Many consumers evaluate affordability using a much narrower standard.

They ask:

“Can I get it?”

Instead of:

“Can I comfortably sustain it?”

This difference explains why financial stress often emerges after major purchases.

The product was accessible.

The financial burden was underestimated.

The affordability illusion causes many individuals to mistake borrowing capacity for financial capacity.

The consequences can persist for years.

Why Spending Decisions Are Often Emotional

Most people like to believe they make rational purchasing decisions.

Research in behavioral finance consistently demonstrates that emotions play a much larger role than many consumers realize.

Purchases often provide psychological rewards such as:

- Excitement.

- Confidence.

- Comfort.

- Recognition.

- Achievement.

- Social acceptance.

These emotional benefits can become powerful motivators.

A person may purchase an expensive vehicle not because transportation is unavailable, but because the vehicle creates feelings associated with success.

Someone may buy luxury goods because they provide confidence or social validation.

Others may spend money during periods of stress, boredom, loneliness, or frustration.

The spending temporarily improves emotional state.

Unfortunately, emotional rewards are often short-lived.

The financial obligations remain long after the emotional satisfaction fades.

This creates a common pattern:

| Emotional Trigger | Spending Response |

|---|---|

| Stress | Retail therapy |

| Success | Reward spending |

| Insecurity | Status purchases |

| Boredom | Impulse buying |

Understanding these emotional influences is essential because financial decisions are often psychological decisions disguised as economic decisions.

The Difference Between Ability to Buy and Ability to Afford

One of the most valuable financial lessons involves understanding the difference between buying power and affordability.

Modern financial systems provide extraordinary purchasing power.

Consumers can often obtain products immediately through:

- Credit cards.

- Financing agreements.

- Installment plans.

- Personal loans.

- Buy-now-pay-later arrangements.

These tools increase access.

However, access does not guarantee financial suitability.

Consider two consumers:

| Consumer A | Consumer B |

|---|---|

| Can finance luxury vehicle | Can finance luxury vehicle |

| Weak savings | Strong savings |

| Limited investments | Strong investment portfolio |

| High financial stress | Minimal financial stress |

Both consumers can buy the vehicle.

Only one may truly be able to afford it.

Millionaires frequently understand this distinction.

Many average consumers do not.

This difference influences countless purchasing decisions throughout life.

The Psychology of Immediate Ownership

Human beings naturally prefer immediate rewards.

Psychologists refer to this tendency as present bias.

Present bias causes people to place greater value on immediate benefits than future benefits.

This explains why immediate ownership can feel incredibly attractive.

The prospect of obtaining something today often feels more compelling than waiting months or years.

Consumers frequently experience thoughts such as:

- “I deserve it.”

- “I’ll worry about the cost later.”

- “Life is short.”

- “Everyone else has one.”

- “I can make the payments.”

These thoughts focus on immediate benefits.

Future financial consequences receive less attention because they feel psychologically distant.

The result is a preference for ownership today rather than financial flexibility tomorrow.

Many expensive purchases are therefore driven not by necessity but by the emotional appeal of immediate possession.

This psychological tendency is one of the primary reasons consumer debt exists on such a large scale.

People often value immediate enjoyment more highly than future financial freedom.

Why Modern Financing Changes Consumer Behavior

Modern financing has transformed consumer behavior in profound ways.

Historically, major purchases often required substantial savings before ownership became possible.

Today, financing allows consumers to obtain products immediately while spreading costs over future periods.

This creates several psychological effects.

First, financing reduces the immediate pain of paying.

Instead of focusing on the total cost, consumers focus on monthly payments.

Second, financing separates ownership from affordability.

People can obtain products before accumulating equivalent financial resources.

Third, financing normalizes debt.

Borrowing becomes an expected part of consumption.

As a result, purchasing decisions increasingly revolve around:

“Can I manage the monthly payment?”

Rather than:

“Is this purchase financially wise?”

This shift fundamentally changes spending behavior.

The focus moves away from total cost and toward short-term affordability.

The result is that many consumers acquire products that would seem far less attractive if full payment were required immediately.

Modern financing is not inherently harmful.

However, it can make expensive purchases feel deceptively affordable.

In the next section, we will examine how social pressure, status consumption, credit cards, monthly payment psychology, and lifestyle expectations encourage people to buy things they cannot afford and how these behaviors ultimately affect long-term wealth creation.

Social Pressure and Status Consumption

Human beings are social creatures.

Much of our behavior is influenced by the opinions, expectations, and perceived judgments of others.

This influence extends deeply into financial decision-making.

Many purchases are motivated not by practical necessity but by social considerations.

People often spend money to:

- Gain acceptance.

- Signal success.

- Avoid embarrassment.

- Improve social standing.

- Meet perceived expectations.

- Demonstrate achievement.

This phenomenon is commonly known as status consumption.

Status consumption occurs when products are purchased primarily because of what they communicate rather than what they accomplish.

The item becomes a social signal.

For example:

- A luxury vehicle may signal success.

- A prestigious address may signal achievement.

- Designer brands may signal social status.

- Premium experiences may signal financial prosperity.

The challenge is that status signals often come with substantial financial costs.

The consumer receives social recognition, but also acquires financial obligations.

When status becomes a primary spending motivation, financial decisions frequently become disconnected from long-term wealth-building objectives.

The result is a lifestyle designed to impress others rather than strengthen financial health.

The Desire to Appear Successful

One of the strongest psychological drivers behind unaffordable purchases is the desire to appear successful.

Success is often judged visually.

People cannot easily see:

- Net worth.

- Investment portfolios.

- Emergency reserves.

- Retirement accounts.

- Financial discipline.

Instead, society often evaluates visible indicators:

- Homes.

- Vehicles.

- Clothing.

- Travel.

- Consumer goods.

Because visible assets receive attention, many individuals focus on creating the appearance of success.

Unfortunately, appearances can be expensive.

The desire to look successful often leads consumers to:

- Upgrade lifestyles prematurely.

- Purchase luxury products.

- Accept larger debt obligations.

- Increase discretionary spending.

From an accounting perspective, appearance and financial strength are entirely different concepts.

A person can appear successful while possessing:

- Large debts.

- Weak savings.

- Limited investments.

- Negative cash flow.

The desire to appear successful often encourages spending that weakens actual financial success.

This contradiction explains why some people appear wealthy while remaining financially fragile.

Keeping Up With Other People

Comparison is one of the most powerful influences on spending behavior.

People naturally compare themselves with others.

Historically, these comparisons were limited to family members, neighbors, colleagues, and local communities.

Today, social media has dramatically expanded the comparison environment.

Consumers are exposed daily to carefully curated images of:

- Luxury vacations.

- Expensive homes.

- High-end vehicles.

- Designer products.

- Premium lifestyles.

This constant exposure can create unrealistic expectations.

People begin evaluating their own lives against highly selective portrayals of other people’s lives.

The result is often dissatisfaction.

Even individuals with comfortable financial situations may feel inadequate.

This feeling can trigger spending designed to reduce perceived social gaps.

Unfortunately, the comparison process never truly ends.

There will always be someone with:

- A larger home.

- A newer vehicle.

- A higher income.

- A more luxurious lifestyle.

Attempting to keep pace with constantly shifting social benchmarks often leads to financial exhaustion.

The pursuit becomes endless because the target continually moves.

Many people buy things they cannot afford because they are unconsciously competing in a race that has no finish line.

The Role of Credit Cards and Consumer Debt

Credit cards have fundamentally changed spending behavior.

Before widespread consumer credit, spending was generally constrained by available cash.

Today, consumers often spend future income rather than current resources.

Credit cards create several psychological effects:

- Reduced spending friction.

- Immediate access to products.

- Delayed financial consequences.

- Less visible payment pain.

Research consistently shows that consumers often spend more when using credit compared to cash.

This occurs because the payment feels less tangible.

The product is received immediately.

The financial cost arrives later.

This separation weakens the psychological connection between spending and sacrifice.

Consumer debt also creates the illusion that lifestyle improvements can occur immediately.

Instead of saving for years, consumers can obtain products today.

The trade-off is future financial obligations.

While responsible credit use can be beneficial, excessive reliance on debt often enables spending beyond sustainable financial limits.

Many consumers do not become financially stressed because of one large purchase.

They become financially stressed because numerous debt-financed purchases gradually accumulate.

Eventually, monthly obligations consume a growing percentage of income.

Financial flexibility begins to disappear.

Why Monthly Payments Hide the True Cost

One of the most powerful techniques used in modern financing is shifting attention away from total cost and toward monthly payments.

Consumers frequently evaluate purchases by asking:

“Can I afford the monthly payment?”

Rather than:

“What is the total financial cost?”

This difference is significant.

Monthly payment thinking often makes expensive purchases appear affordable.

For example:

| Purchase Evaluation Method | Psychological Effect |

|---|---|

| Total Cost Focus | Highlights full financial commitment |

| Monthly Payment Focus | Makes expensive purchases feel manageable |

A luxury vehicle costing tens of thousands of dollars may feel intimidating when viewed as a total purchase.

The same vehicle may appear reasonable when presented as a monthly payment.

This psychological framing changes perception.

The consumer focuses on short-term affordability rather than long-term cost.

Over time, multiple monthly obligations can accumulate.

Individually, each payment appears manageable.

Collectively, they can create significant financial strain.

This is one reason why many people underestimate the true financial impact of major purchases.

The Financial Consequences of Overconsumption

The long-term consequences of buying things that cannot truly be afforded are often more severe than consumers initially realize.

Overconsumption affects more than bank balances.

It affects the entire financial system.

Common consequences include:

- Higher debt levels.

- Reduced savings.

- Limited investment growth.

- Financial stress.

- Restricted future opportunities.

- Delayed wealth accumulation.

Perhaps the greatest hidden cost is opportunity cost.

Every dollar devoted to maintaining excessive consumption cannot simultaneously be used to:

- Build investments.

- Acquire productive assets.

- Reduce debt.

- Increase financial security.

The effects compound over time.

Small financial decisions repeated consistently often produce larger consequences than single major purchases.

Many consumers focus on the benefits of ownership.

They overlook the opportunities surrendered in exchange.

This is why overconsumption frequently delays wealth creation even among individuals with strong incomes.

The issue is not always how much money is earned.

The issue is how much of that money remains available for building future wealth.

In the final section, we will examine how wealth builders think differently about purchases, explore the opportunity cost of expensive consumption, explain why financial discipline creates freedom, and reveal how a wealth-oriented spending mindset helps people avoid buying things they cannot truly afford.

How Wealth Builders Think Differently

One of the biggest differences between individuals who build wealth and those who struggle financially is not income.

It is perspective.

Wealth builders often approach purchases differently.

Instead of asking:

“Can I buy this?”

They ask:

“Should I buy this?”

The distinction is subtle but powerful.

Most consumers focus on accessibility.

Wealth builders focus on consequences.

Before making significant purchases, they frequently evaluate:

- The long-term financial impact.

- The effect on cash flow.

- The effect on savings goals.

- The effect on investments.

- The effect on financial flexibility.

This evaluation process creates a barrier between desire and action.

That barrier often prevents expensive mistakes.

Wealth builders recognize that every purchase has two prices:

- The visible purchase price.

- The invisible future cost.

The visible price appears on the receipt.

The invisible price appears through reduced investments, delayed wealth accumulation, and lost financial opportunities.

This broader perspective often leads to dramatically different financial outcomes over time.

The Opportunity Cost of Expensive Purchases

One of the most overlooked concepts in personal finance is opportunity cost.

Every financial decision eliminates alternative possibilities.

When money is spent in one direction, it cannot simultaneously be used elsewhere.

For example, a luxury purchase may also represent:

- Investments that were never made.

- Debt that was never reduced.

- Savings that were never accumulated.

- Assets that were never acquired.

The challenge is that opportunity costs are invisible.

Consumers see the product they purchased.

They rarely see the future wealth they sacrificed.

Consider a simplified example:

| Option A | Option B |

|---|---|

| Purchase luxury item | Invest the same amount |

| Immediate enjoyment | Future financial growth |

| Value may decline | Value may increase |

| Short-term reward | Long-term benefit |

This does not mean all discretionary spending is wrong.

Rather, it means every purchase should be evaluated in context.

Millionaires often understand opportunity cost intuitively.

Average consumers frequently focus only on the immediate transaction.

The cumulative effect of this difference becomes substantial over decades.

Why Financial Discipline Creates Freedom

Many people view financial discipline as restrictive.

They associate budgeting, saving, and controlled spending with sacrifice.

In reality, financial discipline often creates freedom.

Every avoided unnecessary expense preserves future options.

Every investment contribution increases financial flexibility.

Every debt reduction strengthens financial resilience.

Freedom comes from having choices.

Financial discipline helps create those choices.

For example:

- Emergency savings provide security during uncertainty.

- Investments create future opportunities.

- Low debt levels increase flexibility.

- Strong cash flow reduces stress.

Conversely, excessive consumption often creates dependency.

Higher expenses require higher income.

Higher debt requires ongoing payments.

Financial obligations limit options.

This is why many wealthy individuals embrace discipline.

They understand that temporary restraint can create permanent freedom.

The objective is not deprivation.

The objective is control.

Control over finances frequently translates into greater control over life decisions.

Building a Wealth-Oriented Spending Mindset

A wealth-oriented spending mindset approaches money differently than a consumption-oriented mindset.

The focus shifts from obtaining more products to building stronger financial foundations.

Key characteristics often include:

Prioritizing Ownership

Resources are directed toward assets rather than excessive consumption.

Evaluating Long-Term Impact

Purchases are considered within the context of future financial goals.

Protecting Cash Flow

Maintaining financial flexibility becomes a priority.

Avoiding Lifestyle Traps

Income growth does not automatically trigger proportional spending growth.

Thinking Beyond Immediate Gratification

Future opportunities are valued alongside present enjoyment.

This mindset does not eliminate spending.

It changes the purpose of spending.

Money becomes a tool for creating long-term value rather than merely satisfying short-term desires.

The result is a financial system that grows stronger over time rather than becoming increasingly dependent on income.

Learning to Delay Purchases

One of the simplest and most effective financial skills is learning to delay purchases.

Many expensive mistakes occur because decisions are made quickly.

Emotion is strongest during the initial desire phase.

Time often weakens that emotional intensity.

A delay period creates space for rational evaluation.

Consumers frequently discover that:

- The purchase was not truly necessary.

- The excitement fades.

- A less expensive alternative exists.

- The money can be used more effectively elsewhere.

Many financially successful individuals use deliberate waiting periods before making major purchases.

The objective is not to avoid spending.

The objective is to ensure spending decisions are intentional rather than emotional.

Delaying purchases often produces two benefits simultaneously:

- Fewer unnecessary expenses.

- Greater appreciation for purchases that are ultimately made.

Patience may seem like a small financial skill.

Over decades, it can have a surprisingly large impact on wealth accumulation.

Why People Buy Things They Cannot Afford

People buy things they cannot afford for many reasons.

Some seek status.

Some seek approval.

Some seek comfort.

Some seek excitement.

Others simply underestimate the long-term consequences of their decisions.

The behavior is rarely caused by a single factor.

Instead, it reflects a combination of:

- Psychological influences.

- Social pressures.

- Consumer culture.

- Easy access to credit.

- Present-focused thinking.

Modern financial systems make purchasing easier than ever before.

Access to products has expanded dramatically.

Financial wisdom, however, remains just as important as it has always been.

The ability to obtain something is not the same as the ability to afford it.

This distinction separates many wealth builders from many consumers.

Wealth builders understand that every financial decision affects future opportunities.

They recognize that money spent today influences financial freedom tomorrow.

They evaluate purchases not only by their immediate benefits but also by their long-term consequences.

From an accounting perspective, affordability is ultimately determined by sustainability.

A purchase is truly affordable when it supports rather than weakens financial health.

The individuals who achieve lasting financial success are often those who master this principle.

They learn that financial freedom is not created by acquiring everything immediately.

It is created by making decisions that strengthen their financial position over time.