Once a symbol of the American Dream, college has transformed into a crushing lifetime financial burden for millions, with student debt soaring to $1.7 trillion—a crisis born not from greed, but from deliberate policy shifts: starting in the 1970s, states slashed funding for public universities while federal aid pivoted from grants to loans, forcing students to shoulder costs that had once been shared by society; this fiscal retreat coincided with a powerful cultural myth—that a four-year degree was the only path to success—fueling enrollment and tuition hikes as universities competed for students with amenities like lazy rivers, all financed by easy credit; meanwhile, other nations like Germany (where public colleges are tuition-free) and the UK (with income-contingent loans forgiven after 30 years) treat higher education as a public good, avoiding America’s debt trap, leaving U.S. graduates not just burdened by an average $31,000 loan, but often trapped by unpayable balances, eroded Pell Grants, and bankruptcy protections that make their debt nearly impossible to escape, turning what was meant to be a ladder of opportunity into a cage of intergenerational financial anxiety.

The American Student Debt Quagmire: Why College Became a Lifetime Burden

Once a gateway to the American Dream, a college education has become a lifetime financial burden for millions, with the national student debt soaring to a staggering $1.7 trillion. This crisis was born from a massive policy shift: where public colleges were once heavily subsidized or even free, state funding plummeted starting in the 1970s. To compensate, universities drastically hiked tuition while federal aid pivoted from grants to loans, transferring the cost directly onto students. Fueled by a powerful cultural narrative that a degree was the only path to success, generations borrowed heavily, only to find their debt—now averaging $30,000 per graduate—delaying homes, families, and careers, and creating a weight that can haunt borrowers for a lifetime.

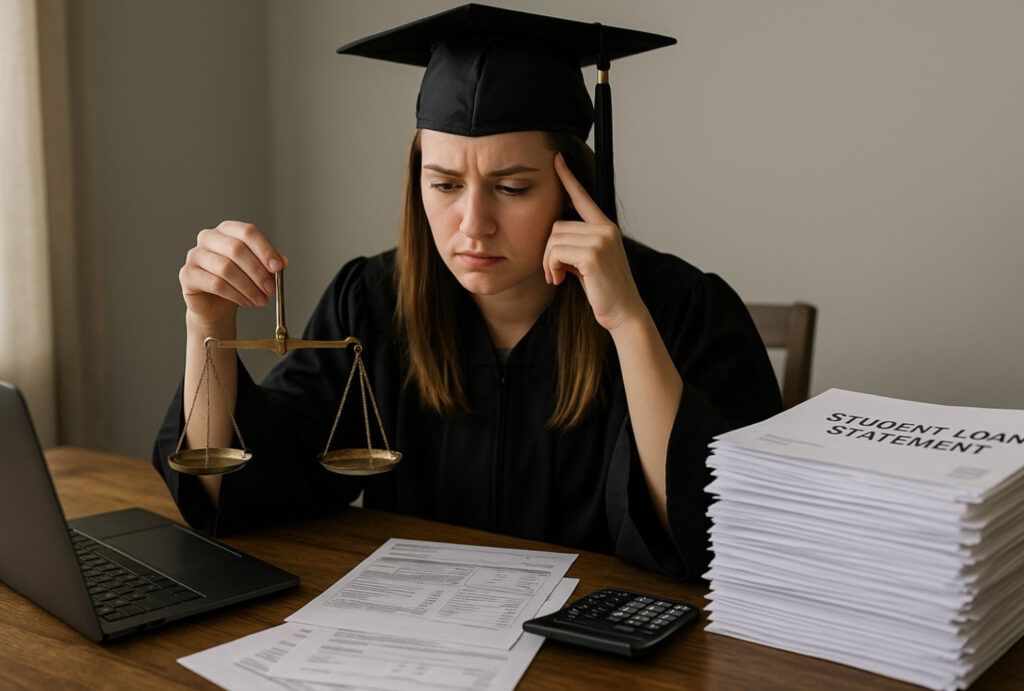

A graduate weighs her future against a mountain of loan bills. In America, the promise of college often comes with a price that graduates carry for years—a burden nations like Germany or China largely avoid by funding higher education as a public good. As the U.S. confronts the student debt crisis, it faces a pivotal choice: continue down the path of personal debt, or invest in making higher education attainable without generations paying for it.

The Cost of a Dream

In the United States, pursuing a college education has long been equated with achieving the American Dream—a gateway to career success and upward mobility. Yet for millions of Americans, that dream comes with a staggering price tag: over $1.7 trillion in collective student loan debt carried by roughly 44 million borrowers. This massive burden has transformed higher education from a public good into a personal financial gamble, one that shapes life choices and haunts graduates for decades. Young adults delay starting families, buying homes, or launching businesses under the weight of loan payments. The average new graduate today owes about $30,000—more than four times the average debt of a graduate in 1990. Monthly payments can devour 10–15% of a borrower’s income, a strain that hits lower earners hardest. How did we get here? To understand why student debt became so crushing in America, we must look to the past, when college was remarkably affordable (even free in some places), and trace the policy shifts, cultural forces, and cost explosions that shifted the burden onto students. We must also examine how other countries—like the UK, Germany, and China—have charted different paths to finance higher education, and what lessons they offer. Finally, we’ll explore fresh perspectives on reforming a broken system, from bold public investments to innovative repayment models, in hopes of easing the generational crisis of college debt.

When College Was Cheap—or Even Free

It may astonish today’s students, but within living memory many U.S. public colleges charged little to no tuition. During much of the 1960s, public universities in states like California were essentially tuition-free for residents. Under California’s famed Master Plan, the University of California and state college systems levied only nominal “incidental” fees; “tuition, as we think about it today, was not an essential part of the financing plan” for in-state students, a UCLA catalog from 1965 proudly noted. That same year, an in-state undergrad’s total annual cost at UCLA was estimated at just $1,710 (about $15,000 in today’s dollars), with no tuition included—students paid only for room, board, and small fees. On the East Coast, the entire City University of New York (CUNY) system operated tuition-free for over a century. CUNY’s flagship, founded as the Free Academy in 1847, upheld its no-tuition tradition until the fiscal crisis of 1975 forced a change. In fall 1976, CUNY imposed tuition for the first time, abruptly ending a 129-year-old free-college policy. Freshmen were charged $650 a year and seniors $800—modest sums even then, but a turning point that would only accelerate in years to come.

These examples weren’t isolated. Many state universities founded in the 19th century as land-grant colleges initially charged no tuition, in line with their mission to broaden educational opportunity. Through the mid-20th century, public higher education was heavily subsidized by state governments and, after World War II, by federal programs like the GI Bill that sent millions of veterans to college at virtually no cost. “Public colleges and universities were often free at their founding… but over time, as public support failed to keep up with growing enrollments and costs, they moved first to low tuition and eventually to high tuition,” explains Cornell higher education professor Ronald Ehrenberg. Indeed, tuition was never zero everywhere—some colleges charged modest fees, and private institutions always set their own rates—but the prevailing ethos was that the public should bear most of the cost of college, not individual students. In 1975, the maximum federal Pell Grant (for low-income students) covered nearly 80% of the average cost of attending a public university, including room and board. A student of modest means could feasibly work a part-time job and graduate with little debt. College, for a brief golden age, was seen as an affordable path to opportunity, broadly accessible to the middle class.

How Students Became the Ones to Pay

Starting in the late 1960s and accelerating through the 1970s and 1980s, this paradigm of low-cost public college collapsed. A confluence of social change and policy choices fundamentally altered who pays for higher education in America. Enrollments surged after WWII and through the ’60s as the baby boom generation came of age and the civil rights movement opened campuses to more diverse students. Demand for college seats exploded – fueled further by a growing cultural mantra that “college is the ticket to success”. But colleges’ capacities and public funding didn’t expand fast enough to meet the influx of students. Instead of doubling down on public investment to maintain tuition-free education, many state leaders began pulling back. The social unrest of the late 1960s also played a role: campus protests and the democratization of higher ed spooked some politicians into questioning generous funding. In California, Governor Ronald Reagan famously railed against the no-tuition policy, arguing taxpayers shouldn’t “subsidize intellectual curiosity” of students; after taking office in 1967, he pushed to impose tuition at state campuses. Reagan’s tuition plan was initially defeated, but the state did hike “registration fees” and began chipping away at the free-college model. By 1982, even California’s community colleges, the last holdouts of zero tuition, started charging students.

On a national level, policymakers shifted financial aid away from grants toward loans, effectively transferring costs to students. The Higher Education Act of 1965 established the first broad federal student loan program, and in 1972, Congress created a quasi-public entity, Sallie Mae, to buy and service student loans—turbocharging the loan market. Loans were touted as a way to expand access without direct government spending, but they introduced a profit motive and future repayment obligation that didn’t exist when aid was predominantly grants. As one analysis puts it, by the early 1970s the stage was set: “States began reducing per-student funding… and state schools began charging tuition for the first time since the Morrill Act”, while the student loan industry took off under the Nixon administration, firmly planting the seeds of the modern debt crisis.

Critically, state governments retreated from funding public colleges over the ensuing decades. In the post-war years and into the 1960s, states poured money into new campuses and covered a large share of operating costs (often 70–80% of university budgets). But after 1970, recessionary pressures, the taxpayer revolt (e.g. California’s Proposition 13 in 1978), and competing budget priorities (like healthcare and K-12 education) squeezed state higher-ed appropriations. The numbers tell the story: as late as 1990, state funding per student was about 140% higher than federal funding per student; by 2015, state funding per student had barely a marginal edge (just 12% above federal support). Essentially, states pulled back and the slack was partly taken up by increased federal aid—mostly in the form of Pell Grants and loans, not direct institutional support. During the Great Recession of 2008–09, state budgets were slashed and public colleges saw deep cuts; a decade later, state spending on higher ed was still $6.6 billion lower (in inflation-adjusted terms) in 2018 than in 2008. To compensate, universities hiked tuition year after year. Household incomes did not keep pace, so students bridged the gap by borrowing more.

Compounding the problem, the buying power of federal grants eroded. The Pell Grant, designed to cover the bulk of costs for low-income students, has failed to keep up with tuition inflation. In 1975, a maximum Pell Grant covered about 79% of the annual cost at a four-year public college; today it covers just 30%. What that means is students from working-class families now routinely exhaust their Pell, then must either come up with thousands of dollars from earnings or, more often, take out loans to fill the shortfall. In 1975 a student could pay remaining costs by working a part-time minimum-wage job ~15 hours a week; in 2023 a student would need over 40 hours a week at minimum wage to cover the difference – essentially impossible while attending classes. The result: debt has become the de facto financing mechanism for higher education.

“College = Success”: A Cultural Script with a Cost

As policy shifts made students shoulder more of the cost, an influential cultural narrative was simultaneously taking hold: college-for-all. From the 1980s onward, American society increasingly sent the message that a four-year college degree was the surest (or only) route to a stable, middle-class life. High schools ramped up college-prep programs; parents, teachers, and politicians preached that any capable student should aspire to a bachelor’s degree. Enrollment in college kept climbing—by 2020, about 36% of 25-29 year-olds had a four-year degree, up from 24% in 1980. This mass pursuit of degrees certainly created opportunities, but it also fueled tuition increases: colleges knew students were highly motivated to enroll, even at higher prices, because their future depended on it. “When college became an end in itself, it became a luxury good,” one observer quipped, noting that the social status attached to the college experience made it more desirable even as it became more expensive. Universities, in turn, invested in amenities and marketing to attract students—sometimes prioritizing campus luxuries and athletics to entice applicants, a trend that drove costs higher. The rise of the infamous campus “amenities arms race” saw features like climbing walls and resort-style dorms (even a “lazy river” water park at one university) become symbols of competition. Such extras, while not the main cause of rising tuition, reflect an era in which colleges felt pressure to offer a full lifestyle experience, and students (enabled by loans) were willing to pay for it.

Perhaps the most pernicious effect of the college-as-panacea narrative was the stigma it attached to alternatives. Vocational training and skilled trades were often demeaned as second-best options, funneling even students who might prefer a different path into four-year colleges. “The desirability implicit in ‘college for all’ had the effect of branding those who did not attend as social Others—viewed as lower-class or failures,” writes Garrison Fathom in Medium, describing how high schoolers came to see skipping college as a recipe for a “life of want”. Fear of being left behind academically, or of missing out on the middle-class lifestyle promised by a degree, led many to enroll in college even if it meant taking on debt beyond their comfort. The cultural script said: any college debt was a “good investment” in oneself. That assumption has been brutally tested in recent years as tuition outpaced wages and many graduates found themselves in debt for a credential that didn’t deliver the income boost they expected. Approximately 32% of U.S. college students do not complete their degree within six years, often leaving with debt but no diploma. These non-completers are in the worst of both worlds: they carry college loans yet lack the degree that might improve their earnings to repay those loans. America’s dropout rate is far higher than in the UK (where only ~11% don’t finish), which underscores how the “college for all” push may be leading some into higher education who either aren’t well-served by academic programs or who face financial and personal hurdles that derail their studies. They still end up with the loans.

Simultaneously, graduate and professional schools expanded and grew more expensive, adding a new layer to the debt burden. Fields like law, medicine, and dentistry now routinely saddle students with six-figure debts, which in turn influences career choices. For example, the average new law school grad owes about $145,000, pushing many toward corporate law jobs for the higher pay, while those who pursue lower-paid public service roles often do so in hopes of eventual loan forgiveness. In short, debt is not only a financial weight but a force steering the directions of young people’s lives and careers. The pressure to earn enough to service loans has psychological costs too: studies by the American Bar Association and others find significant mental health strain tied to debt, with young professionals reporting anxiety and diminished quality of life despite passion for their work.

The Numbers Behind the Crisis

By most measures, the U.S. student debt situation is unprecedented in scale. Americans now owe more on student loans than on credit cards or auto loans, making student debt the second-largest category of household debt after home mortgages. The total balance (federal and private loans combined) sits around $1.75 trillion in 2025, having tripled since 2006. What does this look like for individual borrowers? On average, a bachelor’s degree recipient graduating today leaves school about $31,000 in debt, up from roughly $20,000 two decades ago and under $7,000 in 1990. But averages only tell part of the story: about 14% of borrowers owe $100,000 or more, typically those with graduate or professional degrees. Meanwhile, a sizeable share (roughly one-quarter) owe less than $10,000 – often people who started college but didn’t finish, or who attended community college. These small-balance borrowers paradoxically have some of the highest default rates, since they may lack the income boost a degree provides. The default rate on federal student loans is around 10%, and millions more are in deferment or forbearance, essentially unable to make progress on their loans. Unlike other consumer debt, student loans are uniquely difficult to discharge in bankruptcy (a restriction enacted in 1976 for federal loans and extended to private loans in 2005), meaning borrowers have almost no escape valve if they fall on hard times. The debt can follow someone literally to the grave, with Social Security payments even garnished for unpaid student loans of some seniors.

One insidious aspect of the crisis is interest accumulation. Many borrowers find that even after years of payments, their balance has stayed the same or even grown due to interest. “Every payment I have made has done absolutely nothing” to the principal, one frustrated borrower told a reporter, reflecting a common sentiment among those in income-driven repayment plans where monthly payments often barely cover interest. Before recent reforms, it was common for low-income borrowers to see their balances negatively amortize (increase) over time because their incomes were too low to cover accruing interest. The federal government has been charging interest rates of about 4–7% on student loans in the past decade (varying by loan type and year), which means a graduate with $30k debt might pay $8,000–$12,000 in interest over a 10-year repayment, on top of the principal. For those in extended or income-based plans, the interest can double or triple the total amount paid. Unlike the UK, which caps student loan interest at inflation + 3% and forgives remaining balances after 30 years, the U.S. until recently had no routine forgiveness except for specific programs (like Public Service Loan Forgiveness after 10 years of nonprofit/government work). However, policy is beginning to shift. In 2023, the Biden Administration launched the SAVE plan for income-driven repayment, cutting monthly payments (e.g. borrowers will pay 5% of discretionary income for undergraduate loans, down from 10%) and ensuring that unpaid interest is not charged if you make your monthly payment. This effectively stops balances from ballooning for those in the program. Additionally, balances will be forgiven after 20 years (undergrad) or 25 years (grad) of payments on SAVE. These changes, while technical, are poised to substantially reduce the long-term burden on low- and middle-income borrowers – though critics note they also shift more cost onto taxpayers over time.

Even so, public anger and anxiety over student debt have grown, driving calls for more dramatic relief. In 2022, President Biden announced a plan to forgive $10,000 for most borrowers (and $20,000 for those who received Pell Grants), acknowledging that “student debt is a heavy burden on America’s middle class”. The fact that this one-time cancellation (which was ultimately blocked by the Supreme Court in 2023) was valued at about $400 billion underscores just how large the accumulated debt is. Yet debt forgiveness, while welcomed by borrowers, does nothing to address the root causes of why college became so expensive in the first place. As analysts across the spectrum have pointed out, wiping out today’s debt would, absent deeper reforms, merely clear the decks for the next generation to take on even more. Why is college so expensive now, compared to a few decades ago? The answers include those funding shifts we explored, but also underlying cost drivers within higher education itself. One oft-cited factor is “administrative bloat”—the rapid growth of university staff and administration. Data show that from the 1980s to today, the number of non-teaching staff at colleges rose far faster than enrollment. Universities now employ armies of managers, student services coordinators, diversity officers, compliance staff, etc., which, while often providing valuable support, add to payroll. Administrative costs “have driven tuition higher for decades,” concludes a Heritage Foundation report, noting that non-instructional spending grew at a much higher rate than instructional spending. Another factor is the labor-intensive nature of education: Baumol’s cost disease theory points out that teaching is hard to make more efficient—a lecture that took one hour to deliver 50 years ago still takes an hour today—so productivity gains that lowered costs in other industries don’t translate well to education. Thus, the relative cost of skilled faculty tends to rise over time.

Furthermore, colleges have had to invest in technology, compliance, and student amenities that didn’t exist before. Students expect high-speed internet, modern labs, mental health counselors, recreational facilities, and more. All good things, but all adding costs. Public universities also increasingly rely on tuition from out-of-state and international students, who often pay higher rates, to subsidize in-state students—an incentive to spend on facilities and marketing to attract those full-pay students. For-profit colleges introduced another dynamic in the early 2000s: these institutions often aggressively recruited students (especially lower-income and non-traditional students) with the lure of flexible online programs, only to leave many with hefty debts and non-transferrable credits. The for-profit sector’s abuses (some schools had 90%+ of students taking loans, high default rates, and dubious job placement outcomes) led to crackdowns in the 2010s, but not before contributing substantially to the debt pile and tarnishing the idea of loans as a ticket to a better career.

How Other Countries Tackle College Costs

To fully grasp why America’s student debt burden is so large, it helps to compare how other major countries fund higher education. The experiences of the United Kingdom, Germany, and China offer sharply contrasting models—each with its own trade-offs but notably less severe debt outcomes for students than the U.S. approach.

United Kingdom (England specifically) – In some respects, the UK’s situation looks similar to America’s: tuition at English universities is notoriously high, up to £9,250 per year (about $11,500) for undergraduates, which rivals average public university tuition in the U.S. However, the financing and repayment model in the UK is entirely different. The UK provides all domestic students government-backed loans that cover tuition fees and often living costs. Crucially, repayment is income-contingent: graduates repay 9% of their income above a certain threshold (about £27,000 currently) through the tax system, and any remaining debt is forgiven after 30 years. In effect, the loan functions like an extra tax on earnings for three decades. If a graduate’s income is low, their payments are low (or zero), and interest is subsidized so that unpaid interest doesn’t explode their balance uncontrollably. The typical English graduate now leaves university with over £40,000 ($50,000+) in debt, which actually exceeds the average U.S. bachelor’s graduate debt. Yet British graduates generally do not feel the same kind of acute burden, because monthly payments are manageable and automatically adjusted to income. There’s no equivalent of an American default crisis—indeed, an estimated 70% of UK borrowers will never repay in full before the slate is wiped clean. The cost of that forgiveness is effectively borne by taxpayers. British universities, for their part, are heavily regulated on what they can charge (the £9,250 cap is set by the government) and rely on public funding to subsidize costly programs. The cultural expectation in the UK is still that many (about half) of young people will attend university, but there’s also a robust vocational training system. One key difference from the U.S.: almost all UK students take the loans regardless of family background, whereas in the U.S., about 30% of undergrads don’t use loans because some families pay upfront. That means any broad loan forgiveness in the UK would mainly benefit middle and upper-middle class graduates (since everyone has loans), unlike in the U.S. where debt is more concentrated among lower-income students. In short, the UK has turned student debt into a kind of graduate tax that is automatically collected and broadly shared. The downside is British graduates carry that repayment obligation well into mid-life, and recent policy tweaks (like freezing the repayment threshold, effectively making low earners pay when previously they wouldn’t have) have sparked debate. But serious delinquency or hardship due to student loans is far rarer than in the U.S., by design.

Germany – In Germany, the idea of student debt as a common life experience is virtually non-existent. Public universities in Germany charge little or no tuition for domestic (and even EU) students – generally just token administrative fees on the order of €200 per semester. This is possible because of a deep commitment to higher education as a publicly funded right. Germany actually experimented with tuition in the 2000s: a few states introduced modest tuition (around €1,000 per year) in 2006–07, but protests and political opposition led every state to reverse course. By 2014, all German public universities were tuition-free again. The philosophy, as one German official put it, is simple: “Yes, it’s free – it’s the German taxpayer paying for it. Somebody is footing the bill, just not the student”. That willingness to collectively fund college stems from social values around equality of opportunity and a historical memory of how tuition was abolished in the 1970s during a period of social progress. How do German students cover living expenses? There is a federal aid program known as BAföG, which provides need-based grants and interest-free loans. Initially (1971) it was a full loan for 50% of students; later it evolved to 50% grant, 50% zero-interest loan, and many students today still qualify for some BAföG support. The BAföG loan portion is repaid after graduation, but with generous terms: low or no interest, income-based allowances, and a cap on the total repayment amount. Exceptional performance can even earn partial loan forgiveness (Germany has rewarded top students by forgiving up to 20% of their loan). Moreover, student loan debt in Germany is relatively rare – only about 25% of students take loans nowadays (down from 50% in the 1970s). Many students live at home or work part-time jobs, and there’s a vast system of scholarships from government and foundations. It’s also common that German students take longer to finish degrees but with minimal financial penalty since each additional semester doesn’t cost tuition. The cultural expectation is not that everyone must go to university; Germany has a prestigious dual education system where apprenticeships in trades or industries are an equally respected path. Those who do pursue academia can do so without signing promissory notes for their future. As a result, Germany has virtually no analogue to the U.S. student debt crisis. It does face other challenges (like underfunding leading to crowded lectures or higher taxes), but the notion of young graduates starting life $30k or $100k in the red is unheard of. German policymakers often express befuddlement at the American system: why charge such high tuition and then struggle with loan repayment schemes, instead of directly funding the universities and sparing young people the hardship? The German model underscores that the student debt crisis is not inevitable—it’s the product of policy choices. By choosing to treat higher education as a public good, financed largely by general taxes, Germany avoids saddling individuals with debt and arguably reaps economic benefits of a well-educated workforce unencumbered by loan burdens.

China – China presents a fascinating hybrid case. Under Mao Zedong’s socialist system, higher education in China was completely state-funded and tuition-free. From the 1950s until the 1980s, college students not only paid no tuition, but top students even received stipends, and upon graduation the government assigned them jobs in a planned economy. Only a tiny elite attended university (less than 2% of the age cohort in 1978), so the costs were manageable for the state. However, starting in the 1980s and especially the 1990s, China underwent a dramatic shift known as the “massification” of higher education. To support rapid economic growth and satisfy popular demand, the government expanded college enrollment from under 1 million students in 1997 to over 9 million by 2010 – an astonishing increase. This expansion came with a policy change: tuition fees were introduced in the mid-1990s. By 1997, China moved to a cost-sharing model where students would pay part of the instructional cost. The transition was swift: in 1989, essentially no tuition; by 2004, tuition and fees made up 30% of university revenue. Still, the government kept tuition levels relatively modest and heavily subsidized. Today, a typical public university in China might charge around CNY 5,000 per year (roughly $750) for tuition – higher for certain majors or graduate programs, but the average is about $2,200 per year. This is a fraction of U.S. tuition. There are also scholarships and grants, especially for STEM fields or top scorers on the Gaokao (college entrance exam).

To help those who can’t afford even the moderate fees, China established a government-subsidized student loan system in 1999. These loans are often disbursed through state banks with the government paying the interest during the study period. As of 2023, the program had lent out over ¥400 billion (about $55 billion) to 20 million students. China has been proactive in adjusting this system: recently it raised the borrowing limits and slashed interest rates on student loans to ease burdens. Undergraduate loan caps were increased to ¥12,000/year and interest rates were cut to 0.6 percentage points below the central bank’s benchmark (the Loan Prime Rate). Moreover, amid the COVID-19 economic aftershocks, China temporarily waived ¥2.3 billion in interest and allowed deferred payment for 2023 graduates. Culturally, China places enormous value on university education, and families often save for years to contribute to fees and living costs; it’s common for parents (and extended family) to cover a large portion so that the student graduates debt-free. The concept of taking on debt for school is still relatively new and somewhat avoided if possible. Only about 5 million Chinese students (out of ~30–40 million enrolled) take out loans each year. There is stigma around debt, and many students would rather work part-time or live extremely frugally than borrow. The upshot is that while China now produces far more graduates than the U.S., it has no equivalent student loan crisis. Tuition is kept low by heavy state subsidies; loans are available but interest-subsidized and often forgiven or postponed for those in hardship. By expanding college access gradually and controlling costs, China managed to bring higher education to the masses without introducing the kind of debt traps seen in America. However, there are concerns in China too: the graduate job market is intensely competitive, and a degree no longer guarantees a good job. Underemployment among young grads is high, leading the government to worry about “NEETs” (youth Not in Education, Employment, or Training). Recognizing this, Chinese authorities are actively promoting vocational education and even creating alternatives to the college rat race (for example, encouraging entrepreneurship or skilled trades) to prevent a scenario where millions pursue degrees only to end up jobless and in debt. Still, the average Chinese college tuition of $2,200 (vs. $8,000+ in the U.S.) means those who do borrow accumulate far less debt than their American counterparts. The contrast is striking: student debt is virtually a non-issue in China in public discourse, whereas it’s a defining economic concern for a generation of Americans.

The Lesser-Known Drivers of Student Indebtedness

Beyond the headline explanations—state funding cuts, rising tuition, cultural pressure—lie some lesser-known factors that have quietly exacerbated student debt in the U.S. One is the policy decision to make student loans extremely difficult to discharge in bankruptcy. In the late 1970s and ’80s, spurred by a few anecdotes of doctors or lawyers quickly wiping out student loans via bankruptcy, Congress tightened the rules so that education loans survived bankruptcy except in cases of severe, provable hardship. This means unlike a credit card or mortgage, which can be reset after a bankruptcy, student debt sticks with borrowers no matter what. The intent was to prevent abuse of the system, but an unintended consequence was that lenders (and colleges) could lend more freely, knowing borrowers had virtually no escape. It removed a market discipline that might have otherwise constrained loan volumes or prompted schools to limit price increases for fear students would default en masse. Instead, the federal government guarantees most student loans, and private lenders have confidence even their private loans will remain collectible for life. The result? A moral hazard where colleges face little consequence if their graduates can’t repay loans; the debt can’t be discharged, and Uncle Sam (or loan servicers) will still attempt to collect. Some experts argue that restoring bankruptcy protections would force lenders and universities to be more cautious about loading young people with debt for programs that don’t pay off.

Another under-discussed driver is the Grad PLUS loan program, introduced in 2006, which allows graduate students to borrow up to the full cost of attendance (tuition plus living expenses) with no fixed cap, unlike undergraduate federal loans which have annual limits. Grad PLUS essentially opened the spigot for expensive master’s and professional degrees. Universities realized they could create new graduate programs (often one- or two-year master’s degrees) and charge high tuition, because students could cover it with federal loans regardless of amount. This has led to a proliferation of pricey graduate credentials—some valuable, some of dubious value—and significant debt. For example, a master’s in social work might cost $80,000 in tuition at a private university, leading students to graduate with $100k debt for a field that pays perhaps $50k/year. Why was the student allowed to borrow so much? Because Grad PLUS had no cap and minimal underwriting. The government effectively bankrolled whatever colleges chose to charge. In recent years, calls to rein in Grad PLUS have grown as stories emerged of grads with six-figure debts in fields like psychology, arts, or education, where salaries often don’t match the debt load. Similar criticism has been aimed at Parent PLUS loans, which allow parents to borrow for their children’s college with few limits. Many low-income parents have taken out Parent PLUS loans that they struggle to repay, essentially indebting families across generations.

Moreover, the structure of university finances changed. As public funding shrank, universities embraced privatization strategies: recruiting more out-of-state and foreign students who pay higher tuition, partnering with corporations for research, and relying on adjunct faculty to cut instructional costs. Some public universities now get well under 20% of their budget from state funds (down from 70+% decades ago), the rest coming from tuition and private sources. This marketization arguably made colleges act more like businesses—raising prices, spending on marketing, and even using tuition discounting tactics (charging a high sticker price but giving many students institutional “scholarships” funded by that high price). Private colleges, lacking state funds, also hiked tuition dramatically but then offered steep discounts to attract students; the average private college now discounts over 50% of tuition for first-year students. It’s a price-tag shell game that can confuse families and has steadily ratcheted up the published cost of college. The psychological effect is that many students feel fortunate or “grateful” to only pay, say, $20k at a private college whose sticker price is $50k—when in fact $20k is still a hefty sum often requiring loans. Meanwhile, for-profit colleges, some of which targeted vulnerable populations with aggressive sales pitches about career outcomes, left a legacy of high default rates. At one point in the early 2010s, students at for-profit schools made up about 10% of college enrollment but nearly half of all student loan defaults. Regulatory crackdowns (like the Obama-era “gainful employment” rule) forced many bad actors to close, but the borrowers they left behind still struggle with debts for incomplete or low-quality programs.

Finally, there is the sheer complexity of the student loan system that often works against borrowers. Until recently, there were numerous repayment plans, forgiveness options, deferments, and interest subsidies that were poorly communicated. Many 18-year-olds sign for loans without fully understanding the terms (interest capitalization, for example, which can make unpaid interest become part of the principal, causing interest to then accrue on a higher balance). Financial literacy education hasn’t kept up, and loan servicers have been critiqued for failing to adequately inform borrowers of their rights (like income-driven plans or PSLF). This has led to situations like teachers who could have gotten loan forgiveness after 10 years but didn’t file the paperwork correctly, or borrowers who stayed in hardship forbearance (temporarily pausing payments) without realizing interest was piling up. In sum, a combination of policy blind spots and administrative failures worsened the debt outcomes. Borrowers are now getting more tools (the new SAVE plan, one-time account adjustments to count past payments toward forgiveness, etc.) that should help, but these improvements come after decades of people navigating a byzantine system.

Charting a Way Out: Reform and Relief

If there’s a silver lining to the student debt crisis, it’s that it has sparked a national conversation rethinking how the U.S. finances higher education. A broad consensus has emerged on one point: the status quo is untenable. Americans across the political spectrum recognize that soaring college costs and the resulting debt are inhibiting young people from launching independent adult lives and achieving financial security. The debate now centers on solutions. Here are several paths experts and policymakers are proposing to reduce the burden for future students and repair the system’s flaws:

1. Renew Public Investment in Higher Education: One straightforward (if politically challenging) fix is for the government to pick up a larger share of the college tab again, reducing the need for tuition and loans. This could mean increasing state funding to public universities (so they can lower in-state tuition) or a new federal–state partnership that incentivizes states to waive tuition. The idea of tuition-free public college for at least two years (community college) or even four years has gained traction. In fact, President Obama proposed making community college free; some states like Tennessee and Oregon established “College Promise” scholarship programs to cover community college tuition. More ambitiously, Senators Bernie Sanders and Elizabeth Warren have championed federal plans to eliminate tuition at public colleges for most families, funded by taxes on wealthy households or financial transactions. Historically, remember, this isn’t unprecedented: New York recently launched the Excelsior Scholarship that effectively makes SUNY/CUNY colleges tuition-free for families earning under $125,000 (students must meet certain academic and residency criteria). The key argument for free college is that higher education is a public good that benefits society and the economy, so society should collectively finance it, just as we do K-12 education. Skeptics raise concerns about cost and fairness (should taxpayers who didn’t go to college pay for those who do?), but the counterpoint is that an educated workforce boosts productivity and reduces reliance on social safety nets. Even partial measures, like doubling the Pell Grant (so it once again covers a majority of costs) or funding free community college nationwide, would substantially cut borrowing. Research shows that state disinvestment directly correlates with rising tuition, so restoring funding could reverse that trend. Of course, this requires political will and prioritizing education in budgets, which varies by state.

2. Clamp Down on College Costs and Accountability: Another reform avenue is to address the price of college more aggressively. Policymakers could create incentives or requirements for colleges to rein in tuition growth. One idea is a “College Accountability” framework, where institutions would lose access to federal aid if their graduates consistently can’t repay loans or earn above a certain threshold. Essentially, hold colleges responsible for the outcomes of their students. This concept was partially applied in the Gainful Employment rule (for vocational programs), and some propose extending it to all programs: if an academic program produces graduates with debt-to-income ratios above a set limit, the college might have to pay a fine or risk losing federal loan eligibility for that program. This creates pressure for schools to either improve quality (career services, curriculum relevance) or lower prices to ensure debt is manageable. Another approach is greater transparency: require colleges to provide clear data on average student debt and earnings by major, so students can make informed choices (this is now available via the College Scorecard, but many prospective students are unaware of it). Some reformers suggest capping the amount students can borrow for certain degrees based on expected income, though that’s controversial and could restrict access. At the very least, simplifying college financial aid offers and letting students see a four-year projected cost could prevent surprises. Additionally, tackling administrative bloat and inefficiencies through policy (perhaps capping non-instructional spending growth or encouraging resource-sharing among campuses) is floated as a way to curb tuition hikes. Critics note that heavy regulations could backfire, but there’s momentum for demanding that colleges have “skin in the game”. As one policy group put it, “Real reforms will place accountability on colleges to deliver better value for students and taxpayers, instead of ballooning subsidies that benefit colleges” without cost control. The Biden administration has, for example, announced plans to rank programs by value and warn or even cut aid to the poorest performing ones.

3. Overhaul the Student Loan Repayment System: The U.S. is moving in the direction of income-based repayment by default, and many experts believe that’s key to preventing future crises. One proposal is to automatically enroll all borrowers in an income-driven plan (like the new SAVE) so no one is stuck with a huge unaffordable fixed payment right after graduation. Monthly payments would adjust with income—as in the UK or Australia—and after a set period, remaining debt would be forgiven. The SAVE plan is a big step: it will cut payments for many undergraduates and forgive loan balances after 20 years (for those who consistently earned low incomes, much will be forgiven). However, it’s optional. Making it the default or only plan would simplify things greatly. Furthermore, integrating loan repayment with the payroll tax system (so employers withhold the 5% or 10% automatically, like a tax) could reduce defaults and hassle. Economists note that if loans function more like a “graduate tax,” the psychological burden might lessen—people don’t view it as a debt, more as a time-limited contribution. Another important reform is interest relief: eliminating interest or setting it at nominal rates (0–1%) for federal loans. The federal government currently profits off student loan interest in many years; by zeroing out interest beyond inflation, borrowers could actually chip away at principal when they pay, rather than seeing balances persist. Some bills in Congress have proposed nixing interest and instead charging a one-time origination fee to cover administrative costs. Short of that, expanding subsidies for interest (as was done for undergraduate loans while in school, or currently for some income-driven plan participants) helps prevent the balance balloon effect.

4. Loan Forgiveness and Targeted Relief: While broad jubilee-like cancellation remains politically polarized, there are narrower reforms gaining steam. One is to expand Public Service Loan Forgiveness (PSLF) by making it easier to qualify and automating the process. PSLF, which forgives remaining federal loan debt after 10 years of service in government or nonprofits, was notoriously plagued with mismanagement (98% denial rates at one point). The Department of Education has since fixed many issues and approved over $10 billion in PSLF discharges. There’s bipartisan support for public servants (teachers, nurses, military, etc.) to get relief as a workforce incentive. Similarly, forgiving undergraduate debt after 20 years of payments (which is now codified under SAVE) could be enshrined in law so it isn’t subject to policy whims. Bankruptcy reform has surprising cross-party interest too: a bipartisan bill in 2022 proposed allowing student loans to be discharged in bankruptcy after a 10-year repayment attempt. This would restore a safety valve for the truly struggling and give lenders reason to be more cautious. For those who attended predatory for-profit colleges or were defrauded, borrower defense discharges (already happening) wipe out those illegitimate debts. The Biden administration has approved forgiveness for hundreds of thousands of borrowers from collapsed chains like Corinthian Colleges and ITT Technical Institute. Continuing to police and relieve debts from such bad actors is essential.

5. Innovative Financing Models: Outside traditional loans, some propose alternative ways to fund education. One is the Income Share Agreement (ISA), wherein investors or the school pay a student’s tuition in exchange for a percentage of the student’s income for a set number of years after graduation. ISAs essentially equity-finance a student’s education instead of debt-financing it. If the student earns a lot, the investors do well; if the student earns little, the investors get less (and the student isn’t stuck with a huge fixed debt). A number of coding bootcamps use ISAs, and even Purdue University launched an ISA fund for students. Properly regulated to prevent exploitative terms, ISAs could align the cost of education with outcomes – colleges investing in students’ success because they only get paid if the student succeeds. The Stand Together Foundation (a free-market philanthropy) argues that ISAs and other market-driven models can “mitigate the risk of bad outcomes” by making financing proportional to earnings. There are also employer-driven ideas: employer sponsorship of study (think apprenticeship degrees where a company pays your tuition and you work for them after) or employer student loan repayment benefits. Since 2020, U.S. employers can contribute up to $5,250 per year tax-free to an employee’s student loan payments—this benefit could be expanded or made permanent to encourage more companies to help pay down debt as part of compensation packages. Some large firms and public agencies already use loan repayment as a recruitment tool. Additionally, communities and states have tried “talent retention” programs that forgive or repay loans for graduates who settle in certain areas or enter high-need professions (for instance, STEM graduates who commit to work in a rural region). While these are small-scale, they hint at creative solutions tying education funding to workforce development.

6. Embrace Multiple Education Pathways: A more philosophical but important shift is to move beyond the one-size “college for all” mindset. Policymakers are now talking about investing in career and technical education, apprenticeships, and certificate programs that can lead to good jobs without a four-year degree. If society offers robust, respected alternatives, fewer students will feel compelled to enroll in four-year colleges by default (and taking loans to do so) when another path might suit them better. For example, expanding Pell Grants to cover short-term programs or trade schools can help people skill up without incurring debt. The stigma of not having a bachelor’s needs to be addressed; public messaging and funding should elevate the stature of trades and two-year degrees. In recent years, some states have begun covering tuition for vocational training and apprenticeships just as they would for academic degrees. The goal is to ensure people can achieve livelihoods without necessarily accumulating debt for a BA if that’s not the right fit. Ironically, even some college graduates now turn to trades – stories abound of grads going to coding bootcamps or electrician apprenticeships after struggling in the white-collar job market. This trend reflects how rigidly channeling everyone into college has misallocated talent and left many with debt but mismatched employment. Broadening the definition of educational and career success could alleviate pressure on the loan system by reducing unnecessary credential-chasing.

7. Strengthen Counseling and Financial Literacy: Finally, a low-cost yet impactful reform is to greatly improve the guidance given to students before they take on loans and while they are in school. Many 17-year-olds choose colleges and sign loan promissory notes with only a cursory online entrance counseling session. Schools could be mandated (and funded) to provide one-on-one financial aid counseling, including projections of future monthly payments under various scenarios. Students should be informed of what the typical graduate in their major earns and what their debt-to-income ratio might be. This doesn’t mean discouraging borrowing, but ensuring informed consent. Likewise, on-campus financial literacy programs can help students budget and perhaps borrow less. Some colleges are experimenting with small “completion grants” – micro-grants to help seniors finish up without resorting to last-minute loans or dropping out due to a $1,000 bursar hold. Such interventions recognize that not all debt is created equal; a bit more grant aid at critical moments can prevent a spiral into deeper debt.

In reality, no single reform will solve a problem as large and complex as the student debt crisis. A combination of approaches will be needed: controlling college costs, reimagining funding, protecting students from bad debt, and helping borrowers manage repayment. The encouraging news is that the conversation has shifted from “Is there a crisis?” to “How do we fix this crisis?”. That in itself is progress.