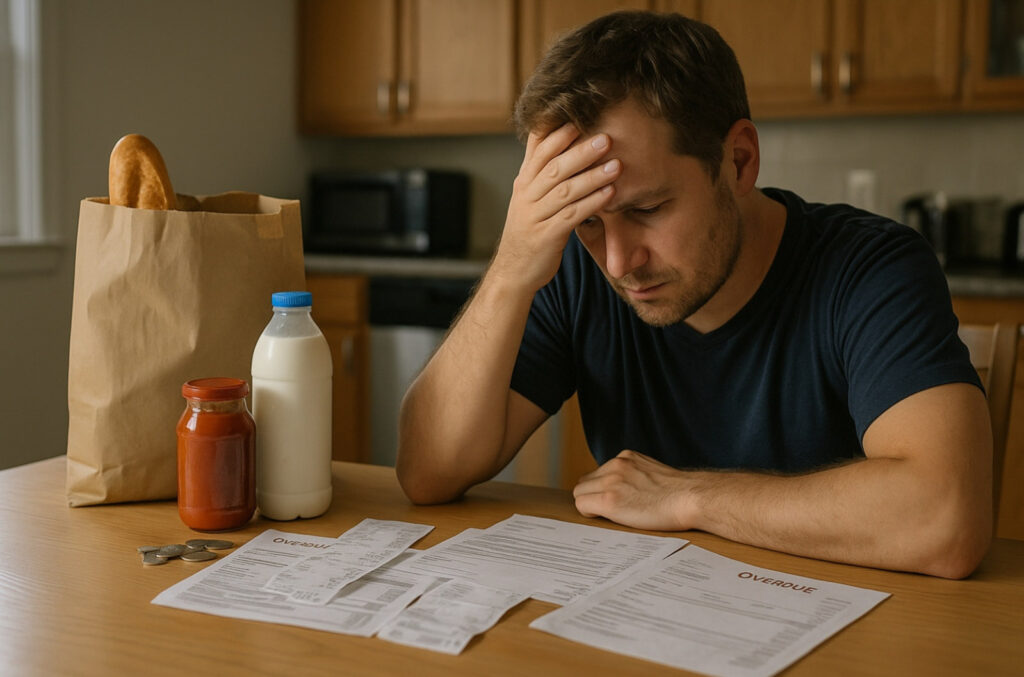

Being poor in America comes with a steep and often hidden price tag. It’s a cruel paradox: people with the least money frequently end up paying more for basic goods and services than those who are better off. From higher interest rates and fees in banking, to inflated prices at the corner store, to costly health and transportation hurdles, the poor face a “poverty penalty” at nearly every turn. These extra burdens act like a hidden tax on low-income families, siphoning away precious dollars and making it even harder to get ahead. As the old saying (and a famous boots analogy) goes, a poor man who can only afford cheap boots ends up spending more over time than a rich man who buys quality boots once. In myriad ways, being poor isn’t just hard – it’s expensive, and it can trap families in a self-reinforcing cycle of poverty.

Consider a working parent trying to make ends meet on a low wage. On paper, they earn too little to afford life’s basics comfortably. But in reality, they may also spend more for those basics than a wealthier family: paying to cash each paycheck because they lack a bank account; paying higher per-unit prices for groceries at a convenience store in their neighborhood; paying exorbitant interest on a short-term loan when the car breaks down; and paying the price of delayed medical care because insurance is out of reach. These kinds of scenarios are daily reality for millions of Americans. Below, we investigate the key areas where the poverty penalty hits hardest – banking and credit, housing, food, healthcare, and transportation – and ask why poverty in America so often seems to punish people with extra costs. We’ll also explore how these burdens reinforce poverty, what might be done to ease this “tax on being poor,” and how the situation in the U.S. compares to other countries.

Banking and Credit: The High Cost of Financial Exclusion

“It costs money to be poor,” the saying goes, and nowhere is that more evident than in the world of banking and credit. Wealthier Americans typically enjoy free checking accounts, low interest rates, and credit cards that earn rewards. By contrast, low-income Americans often face a gauntlet of fees and high interest just to manage their money. Many are “unbanked” or “underbanked” – lacking a basic bank account or relying on alternative financial services. Approximately 5 to 6 million U.S. households have no checking or savings account at all, and roughly 19 million more are underbanked (using services like check-cashing stores or payday lenders despite having a bank account). The reasons vary – some can’t meet minimum balance requirements or mistrust banks – but the outcome is the same: they must turn to cash transactions and fringe services that come at a steep price.

Check-cashing stores and money orders drain funds: Without a bank account to deposit paychecks or pay bills, people often use check-cashing outlets, which typically charge a percentage of the check’s value (often around 1% to 3%). That may sound small, but over time it adds up. For a full-time worker living paycheck to paycheck, paying perhaps $10 or $20 every time they cash their weekly pay, this could mean hundreds of dollars lost per year just to access their own earnings. A Brookings Institution study found that an unbanked worker could spend as much as $40,000 over the course of a career on fees to cash checks and buy money orders – money that a middle-class worker with direct deposit keeps in their pocket. If that $40,000 were instead saved and invested over decades, it could have grown to several hundred thousand dollars in wealth. In short, the poor pay dearly for basic financial transactions that are virtually free for others.

Sky-high fees and interest for small loans: When the bank account is empty and an emergency strikes – the rent is due or the electricity might be shut off – affluent families might whip out a credit card or tap an emergency fund. Poor families often have no such options, forcing them into expensive debt. Payday loans are a prime example. These short-term loans, often for a few hundred dollars, charge astonishing fees that equate to annual interest rates of 300% to 500%. The typical payday loan is about $300-$400, meant to be repaid in two weeks. But many borrowers can’t pay on time and end up renewing or rolling over the loan repeatedly. According to research by the Pew Charitable Trusts, the average payday borrower ends up indebted for five months and pays about $520 in fees for borrowing $375 – effectively spending far more in interest than the original loan amount. It’s easy to see how this “debt trap” keeps people poorer. Similarly, those with tarnished credit might turn to auto-title loans or pawn shops, which also charge hefty fees and can seize vital assets (like a car) if the borrower can’t repay. In total, Americans spend billions each year on high-cost short-term loans – about $9 billion annually on payday loan fees alone – overwhelmingly paid by low-income communities.

Bank fees and overdrafts hit those with the least cushion: Even for low-income people who do have a bank account, staying in the system can be costly. Big banks increasingly require minimum balances (for example, keeping at least $1,500 in an account) or they charge monthly maintenance fees that typically range from $5 to $15. If you can’t meet the minimum – as many living paycheck to paycheck cannot – you get dinged with fees every month. One of the most expensive bites is the overdraft fee. If an account goes negative even briefly (say, a timing mismatch where a paycheck hasn’t cleared but the rent check did), the bank will charge an overdraft fee averaging around $35 per incident. This can turn a small purchase into a big expense. For instance, as one analyst noted, “A $3 cup of coffee can end up costing $38 if it triggers an overdraft.” Banks collected an estimated $14 billion in overdraft fees in a recent year, and those fees overwhelmingly come from lower-balance, lower-income customers. Essentially, the poorest customers – those most likely to overdraft – are subsidizing the banking system with these charges. By contrast, wealthier customers not only avoid overdrafts (thanks to higher balances and cushion) but even earn interest and rewards on their accounts.

Credit card perks for the rich, hurdles for the poor: Access to credit is another arena where the system favors the well-off. Consumers with strong credit scores and higher incomes are courted by credit card companies with low interest rates, no annual fees, and generous cash-back or travel rewards. Meanwhile, people with low incomes or blemished credit often either can’t get approved for traditional credit cards or only qualify for “subprime” credit cards that charge high interest (20%+ APR) and fees. In fact, some subprime credit cards aimed at people with poor credit charge annual fees and monthly service fees that can total over 10% of the card’s small credit limit – essentially a huge extra cost for borrowing a small amount. Furthermore, because many low-income Americans rely on cash or debit instead of credit, they miss out on the rewards that wealthier credit card users enjoy. This has created a perverse situation where every time someone pays cash or debit (common among the poor), a portion of that sale effectively funds the credit card rewards (enjoyed mostly by higher-income people). Economists at the Federal Reserve Bank of Boston estimated that each year, households that use credit cards effectively receive an indirect subsidy of over $1,000 on average, paid for by those who can’t or don’t use credit. In other words, the way our payment system works, the less money you have, the more you end up paying – just to use money.

Between banking fees, high-cost loans, and lost opportunities, the financial services system often works against the poor. As a result, low-income Americans pay thousands of dollars more over time for services that others get essentially for free or at low cost. This not only drains their limited income, but also makes it harder to save and build the financial cushion needed to escape this cycle. Being outside the financial mainstream or on its harsh fringe is like carrying an extra weight in every transaction, ensuring that a dollar in a poor American’s hand simply doesn’t go as far as a dollar held by someone more affluent.

Housing: Paying More for Less

Housing is typically the largest expense for any family – but for poor Americans, it comes with painful trade-offs and hidden costs that wealthier households often avoid. Low-income families generally have two options: pay high rents for substandard housing in low-income neighborhoods, or live far from job centers in search of cheaper rent (incurring other costs like long commutes). Either way, they often get less for more. A common measure is “housing cost burden,” and the statistics are sobering: about 70% of extremely low-income renter households in the U.S. spend more than half of their income on housing costs. By comparison, the average higher-income household might spend well under 30% of income on housing. This means the poor have almost no breathing room in their budgets – and yet the housing they can afford is often overcrowded, in disrepair, or in unsafe neighborhoods. Alarmingly, research suggests that in some respects, poor renters are actually charged higher effective prices for housing than wealthier people pay.

High rents in low-income neighborhoods: It may seem counterintuitive, but landlords in many high-poverty areas charge rents that are disproportionate to the value or quality of the property. A landmark study by sociologist Matthew Desmond found evidence of systematic “housing exploitation” in low-income communities. In better-off neighborhoods, rents generally align with property values – for example, a landlord might recoup the value of a property in about 15–20 years of rent. But in very poor neighborhoods (where many residents live below the poverty line), Desmond found landlords often recoup the property’s value in as little as 4 to 7 years of rent. In one stark comparison, neighborhoods with poverty rates under 15% had an average rent-to-property-value ratio implying about a 10-year payoff period for landlords, whereas in neighborhoods with 50%+ poverty, the ratio was about 25% per year – a property’s cost could be paid off from rent in just four years. In plainer terms, low-income tenants are paying a lot for very little. They often face monthly rents not much lower than those in better neighborhoods, despite having to endure leaky plumbing, mold, pests, broken heating, or dangerous surroundings. Those higher relative rents translate into significant profits for landlords in poor areas – one study found that nationally, landlords in low-income neighborhoods take home higher average monthly profits than those in more affluent areas. In Milwaukee, for instance, landlords in poor neighborhoods were making roughly double the monthly profit per unit compared to landlords in upscale parts of the city. The “slum housing” business can be quite lucrative, precisely because desperate tenants have nowhere else to go and little power to negotiate.

No wealth-building, high instability: Beyond paying a premium for subpar housing, poor families who rent gain no equity for all the money they spend. Middle-class families often buy homes, and over time their mortgage payments effectively turn into ownership of a valuable asset. Homeowners also benefit from rising property values and various tax advantages. In contrast, lifelong renters (disproportionately low-income) can spend decades making rent payments and end up with no asset to show for it. For example, a family paying $800 a month in rent (a modest amount in many regions) will pay nearly $10,000 in a year, and over 10 years that’s $100,000 gone into someone else’s pocket. If that same amount were paying down a mortgage, the family would likely own a sizable chunk of property; but as rent, it builds no wealth for the tenant. This lack of equity is a key reason why poverty persists across generations – poor parents can’t pass down a home or wealth to their children, only the instability of the rental market. And instability is another cost: evictions and frequent moves are common in low-income housing. An unexpected expense or a missed paycheck can mean falling behind on rent and facing eviction. Evictions come with moving costs, job disruptions, kids switching schools, and often having to accept even worse housing thereafter (since an eviction can tarnish tenant records). All of these side effects have financial and social costs that keep poor families on a stressful treadmill.

Utility costs and living conditions: Poor-quality housing can also mean higher utility bills and health costs. Old, inefficient appliances and poorly insulated buildings (common in cheaper rentals) lead to higher electricity and heating bills – so a low-income family might pay more for energy per square foot than a wealthier household in a modern home. If the landlord doesn’t cover utilities, this adds to the monthly burden. Substandard housing can also directly impact health: issues like mold, lead paint, or lack of heat can cause chronic health problems (asthma, lead poisoning, etc.), which then result in medical expenses and lost work days. Wealthier families seldom have to weigh the risk of their home making them sick, but it’s a reality for many low-income renters.

In sum, America’s housing market often forces the poor to pay more than they can afford for less than they deserve. By devoting an enormous share of their income to rent, low-income families forfeit opportunities to save or invest in education, businesses, or other avenues that could improve their lot. High rents, no equity, and exploitative conditions form a vicious cycle: they drain resources from the poor and contribute to keeping them poor. Safe, affordable housing is a cornerstone of financial stability; without it, the poor face yet another uphill battle.

Food Deserts: Higher Prices for Groceries

A trip to the grocery store is a routine errand for many Americans, but for those living in “food deserts” or low-income areas without supermarkets, getting affordable, healthy food is a major challenge. The term food desert describes neighborhoods (often urban low-income areas or rural communities) where residents have little to no access to supermarkets or large grocery stores within a convenient distance. Instead, people must rely on small corner stores, gas station markets, or fast-food outlets for most of their food. The poverty penalty here is two-fold: not only is the selection of healthy food limited, but the prices of everyday food items are often higher than in wealthier areas with big grocery chains. This means low-income families frequently pay more for less nutritious food, which can harm both their finances and their health.

Higher prices at corner stores and small markets: It’s well documented that buying food at convenience stores or bodegas is more expensive per item than shopping at a large supermarket. Big grocery stores benefit from economies of scale and can offer lower prices and bulk deals, but small neighborhood shops have higher supply costs and markups. For example, a USDA study found that staple foods cost significantly more at corner stores: milk might be priced about 5% higher, bread 10% higher, and cereal 20–25% higher than at a supermarket. Other research has found an even wider gap: in some inner-city neighborhoods, residents shopping at small local stores pay anywhere from a few percent up to 30% more for the same products compared to shoppers at suburban supermarkets. Practically, this could mean a gallon of milk that sells for $2.50 at a suburban Walmart might cost $3.00 or more at the only corner shop in a low-income area. A bag of apples or a dozen eggs might be substantially pricier, if they’re available at all. For a family on a tight budget, these higher prices force painful trade-offs: do you spend extra for healthy items, or do you buy cheaper, filling foods with lower nutritional value? Often, the answer skews toward the latter, which leads to another aspect of the poverty penalty in food.

Lack of healthy options and long-term costs: Food deserts don’t just make food more expensive; they also push people toward unhealthy diets. When fresh produce, whole grains, and lean meats are scarce or costly, families understandably turn to what’s available and affordable – typically processed foods, snacks, and fast food. A fast-food dollar menu or a convenience store snack may provide a cheap meal, but a diet built on these options can result in obesity, diabetes, heart disease, and other costly health conditions down the line. In this way, the cost of being poor shows up later in doctor’s bills and lost years of healthy life. Studies have found higher rates of diet-related diseases in communities with poor food access. For instance, neighborhoods identified as food deserts often have obesity and diabetes rates significantly above the national average. One analysis in Chicago found that the death rate from diabetes in food desert areas was twice as high as in areas with grocery stores. The immediate cause is diet, but behind that is the economic reality: healthy eating is harder and more expensive when you’re poor. It’s not uncommon for low-income parents to skip meals or choose cheaper, filling options (like boxed mac and cheese or canned pasta) to stretch their food budget, sacrificing nutrition for calories. Over time, those choices contribute to serious health problems – another facet of how poverty’s “expense” is paid.

The burden of distance and time: Some low-income families try to circumvent food deserts by traveling to distant supermarkets – but that comes with costs too. If you don’t own a car (common in poor urban areas), you might have to take multiple buses or pay for a taxi/Lyft to haul groceries. This adds transportation costs and can turn a simple grocery run into a half-day ordeal. Many families simply cannot do this regularly. Instead, they end up shopping in their neighborhood despite the higher prices. They may also buy groceries in smaller quantities (because they can’t carry bulk items on the bus, or don’t have the cash on hand for a month’s supply at once). Buying food in small increments or single servings is almost always more expensive per unit than buying in bulk. For example, purchasing individual small bottles of juice or single rolls of toilet paper at the corner store will cost far more, over time, than buying a big carton of juice or a multi-pack of toilet paper at Costco – but the poor often don’t have the luxury of bulk buying. It’s a vicious cycle: lacking money and storage, you can’t stock up at low cost, so you pay more frequently for smaller sizes. And if a family manages to get to a supermarket infrequently, they may not have reliable refrigeration or storage at home (another often overlooked issue in substandard housing), meaning they can’t keep fresh food for long.

The upshot is that simply putting dinner on the table can cost more effort and money for a poor family than for a middle-class one. Over a month, the extra dollars spent on each grocery trip in a food desert might mean the family runs out of food before the next paycheck, or has to rely on emergency food pantries to supplement – further stress and instability that wealthier families seldom experience. “Food insecurity” (limited or uncertain access to enough food) often goes hand in hand with these higher costs. It’s a painful irony: America produces an abundance of food, yet millions of its poorest citizens live in neighborhoods where affordable, healthy food is the hardest to find. The poverty penalty here is paid in cash at the register and in health over the long run.

Healthcare: When Prevention is a Luxury

In the United States, getting sick or injured can be financially catastrophic – and once again, those least able to afford it often end up paying the most. Unlike many wealthy countries, the U.S. does not have universal healthcare, and even routine medical care can carry hefty out-of-pocket costs. For people with comfortable incomes and good insurance, this is less of an issue; they can afford copays, and they typically have access to preventive care that catches problems early. But for low-income Americans – especially those without health insurance or with minimal coverage – the healthcare system poses a daunting choice: avoid or delay care and hope for the best, or seek care and risk bills that could wreck their finances. Many end up postponing care until small problems become big ones, leading to emergency room visits or hospitalizations that cost far more (to both the patient and the system) than early treatment would have. In effect, poverty makes healthcare more expensive and health outcomes worse, creating a vicious cycle of poor health and financial strain.

Skipping care due to cost: Surveys have consistently shown that a significant share of Americans – especially those with low incomes – forego medical treatment because of the cost. In recent polls, roughly one-third of U.S. adults (and an even higher fraction of uninsured adults) reported skipping dentist visits, doctor appointments, or recommended medical tests because they could not afford them. Among uninsured adults, nearly half say that basic healthcare is financially out of reach. For someone earning near the poverty line, even a $30 clinic copay or the cost of a prescription can mean the difference between paying the utility bill or not. So they delay. But minor health issues, if untreated, often snowball into major issues. The toothache that went ignored because seeing a dentist was too expensive can become a raging infection requiring an ER visit or an extraction. The high blood pressure that went unmedicated for years could lead to a stroke, with massive costs for hospitalization and rehabilitation. This is the poverty penalty in healthcare: an untreated problem today turns into an emergency tomorrow – with a price tag many times larger.

Emergency rooms as primary care and huge bills: For many uninsured or underinsured poor Americans, the hospital emergency department becomes the fallback source of care. By law, ERs must treat patients regardless of ability to pay, so people in a health crisis (who may have postponed routine care) end up there as a last resort. Emergency care, however, is the most expensive kind of care. A visit to the ER for something like an asthma attack or a severe infection can cost thousands of dollars. If admission or surgery is required, the bills can soar into the tens or hundreds of thousands. Hospitals do provide charity care or write off some of these costs, but often patients are billed and hounded by collections. Medical debt is shockingly common: over 60% of uninsured adults report owing money for medical bills. Even among those with insurance, medical debt is prevalent because of high deductibles and copays – but the uninsured are the most vulnerable. A single health crisis can wipe out whatever meager savings a poor family has, or push them into bankruptcy. Indeed, studies over the past decade have found that medical issues (either high bills or loss of income due to illness) contribute to a large share of personal bankruptcies in the U.S. – by some estimates, as many as half of all bankruptcies have a medical cause or significant medical debt involved. This is virtually unheard of in other developed countries. It’s a uniquely American burden that disproportionately falls on the poor and uninsured.

Worse outcomes and higher long-term costs: There’s a grim logic to how poverty and health costs reinforce each other. Because being poor often means no health insurance (or coverage gaps), people wait until they are extremely sick to seek help. By then, treatments are more complex and expensive, and recovery might be harder. If a person can’t afford medications to manage a chronic condition like diabetes or asthma, they may suffer complications that require ambulance rides and ICU stays – traumatic and costly events that could have been prevented with a steady supply of $50/month medication. Moreover, poor health can then jeopardize someone’s ability to work, leading to lost income and even deeper poverty. For example, imagine a low-wage worker who doesn’t have paid sick leave and avoids going to the doctor for a painful infection. Eventually the pain becomes unbearable and they end up hospitalized for a week – they not only incur a huge hospital bill, but also lose a week’s wages or even their job. Recovering financially from that is exceedingly hard when you have no cushion. The broader community also pays for this inefficiency: emergency care for the uninsured often ends up indirectly paid by taxpayers or through higher costs elsewhere in the system. In short, our healthcare structure often transforms poverty into poor health, and then back into greater poverty. While a wealthier person might treat health as a manageable life aspect (with checkups, medication, and insurance protection), a poor person experiences health as a high-stakes gamble – one they are likely to lose at great expense.

It’s important to note that public programs like Medicaid do provide healthcare coverage for many low-income Americans, and the Affordable Care Act has reduced the uninsured rate. These safety nets help, but gaps remain – millions still fall through, especially in states with limited Medicaid coverage. Even with insurance, the poorest often struggle with things like co-pays, uncovered services (like dental, vision, or certain medications), and the logistical costs of accessing care (finding transportation to a clinic, taking unpaid time off work to sit in a waiting room, etc.). When survival is a daily challenge, focusing on preventive care feels like a luxury. Thus, being poor in America doesn’t just mean having less money – it can mean being effectively shut out of the front door of the healthcare system, only to be let in through the emergency exit at a much higher price.

Transportation: Stranded by Costly Choices

America’s transportation infrastructure often assumes that you have a car. In many communities, especially outside big cities, a reliable automobile is essential for reaching jobs, schools, stores, and healthcare. But owning and maintaining a car is expensive – and that expense hits the poor particularly hard. If you’re well-off, you might buy a new or certified-used vehicle with a low-interest loan, and you can easily afford insurance, gas, and repairs. If you’re poor, you likely can’t afford a new car (which, despite a higher sticker price, often has lower upkeep costs). Instead, you might buy an old used car outright or from a “Buy Here, Pay Here” lot. These options come with a host of hidden costs: high interest payments, frequent repair bills, higher insurance premiums, and a greater risk of breakdowns that can jeopardize your job. And if you don’t have a car at all, you face the cost of inconvenience: lengthy bus rides (where available), expensive ride-share trips in emergencies, or simply missing opportunities because you can’t get there. In short, the transportation system in much of America imposes another poverty penalty – you either pay more to keep clunkers running or you pay in the currency of time, safety, and lost opportunity.

Predatory auto financing and subprime loans: A car is often the largest purchase a low-income household makes. Without good credit, though, financing that purchase can be staggeringly expensive. Many poor buyers resort to “Buy Here, Pay Here” dealerships that specialize in subprime customers. These lots not only charge above-market prices for used cars, but also typically issue loans with interest rates commonly around 20% or higher (often near the legal maximum, which in some states can be 25-30% APR). For perspective, a buyer with excellent credit might finance a car at, say, 5% interest, while a subprime borrower at 25% pays many times more in interest over the life of the loan. That can add thousands of extra dollars paid just in finance charges. Worse, the cars sold to poor buyers are often older models with limited warranties. If the car breaks down and the owner misses work or can’t afford repairs, they might default on the loan – the dealer repossesses the car (then often resells it to the next customer) and the hapless buyer loses whatever they paid. It’s not uncommon for low-income individuals to go through a series of used cars in a short span, each time losing money. In contrast, a wealthier person might buy a reliable car that lasts for many years or lease a new car with full warranty, avoiding most repair costs. Thus, the poor often pay more for transportation in a revolving-door fashion: repeatedly sinking money into high-interest loans for unreliable vehicles.

Insurance and other ownership costs: Car insurance is another area where being poor can literally raise the price. Insurers in most states use credit history as a factor in setting premiums – and a low credit score (which often correlates with low income) can dramatically inflate your insurance rates, even if you have a clean driving record. Analyses by consumer advocates have found that in some cases, a driver with poor credit may pay double or triple the insurance rate of an identical driver with excellent credit. In certain states, a driver with poor credit might even pay more for insurance than someone with a DUI conviction but great credit. This practice effectively penalizes people for being financially insecure. So a low-income driver, already stretched to afford car payments, also gets hit with higher monthly insurance bills (or, worse, they might forego insurance, which is illegal and risky, but sometimes people feel they have no choice). Additionally, poor neighborhoods often have higher auto insurance premiums due to factors like higher theft rates or lack of garages, compounding the cost for residents there.

Maintenance, gas, and the cost of an old car: If you can only afford an older used car, chances are you’ll face more frequent repairs and lower fuel efficiency. Repair bills can be sporadic but devastating – a $600 brake job or a $1,200 transmission fix can upend a tight budget. Wealthier car owners might just pay these and move on, or preemptively maintain their cars. Poorer owners might delay needed fixes (driving on bald tires or with the “check engine” light on) because they lack the cash, which can lead to bigger problems (a blown tire on the highway, or a small engine issue turning into a major breakdown). Some end up abandoning a repair because it exceeds the car’s value, leaving them without transportation at all. Furthermore, older cars and cheap models typically get worse gas mileage. Spending, say, $20 on fuel might get a low-income driver fewer miles of travel than the same $20 gets a wealthier driver with a fuel-efficient car. Over time, these differences nibble away at whatever money is available.

No car, no job: the opportunity cost of poor transit: For those who cannot afford a car at all, the consequences can be even more severe. Many U.S. cities and towns have inadequate public transportation, especially outside urban cores. A low-income person without a vehicle might be effectively barred from jobs that are beyond a bus line or outside of the limited transit schedule. They might have to turn down higher-paying work because they simply can’t get there reliably. If they do rely on public transit, they pay in time: what might be a 20-minute drive for someone with a car could be a 1.5-hour commute with multiple transfers for someone taking buses. That is time not spent earning money, helping kids with homework, or taking a needed rest. It’s an exhausting tax on their day. And if an emergency happens (say, a sick child at school or a relative in the hospital), not having a car can mean expensive alternatives – like hailing a taxi or ride-share last-minute, which can be prohibitively costly from low-income areas or at off-peak times. Some families have to routinely spend money on cabs to get groceries or go to appointments because there’s no other way – an expenditure wealthier households never have to consider.

All told, whether owning an old car or struggling without one, the poor often pay more in the transportation realm. They either pour money into aging vehicles and high insurance, or they sacrifice time, safety, and opportunities by being at the mercy of insufficient transit. Reliable transportation is a lifeline to economic stability – it affects what jobs you can take and what resources you can access. When that lifeline itself is more expensive or fragile for the poor, it further cements the divide. In a country built for cars, not having equal access to affordable mobility is yet another way poverty exacts a higher price.

The Self-Reinforcing Cycle of Poverty

The examples above – in finance, housing, food, healthcare, and transportation – all illustrate a common theme: poverty in America is often self-reinforcing because of systemic cost burdens. In practical terms, being poor means that each dollar you have buys you less of what you need, because you’re paying extra along the way. Meanwhile, the consequences of not being able to pay upfront (whether it’s going without preventative healthcare or driving a worn-out car) lead to even larger expenses later. This creates a cruel feedback loop. The additional costs (the “poverty penalties”) eat away at any progress a family might make. Money that could have been saved or invested in improving one’s situation instead goes to fees, high interest, and emergency expenses. With no savings, any setback – an illness, a car breakdown, a missed paycheck – quickly becomes a crisis, plunging the family deeper into the hole. Sociologists sometimes call this a “poverty trap,” where escaping poverty isn’t just a matter of working harder or earning a bit more, because structural forces keep dragging you back down.

These hidden taxes on poverty also compound one another. A person facing high rent burden likely also has food insecurity, which can lead to health issues, which then might cause them to miss work or incur medical debt, which then hurts their credit, making their car insurance and loans more expensive – and so on. For example, imagine a single mother in a low-income neighborhood: She pays a premium for her apartment but lives in a rough area. She doesn’t have a grocery nearby, so she spends extra at the convenience store and her family’s diet suffers. Her old car frequently breaks down, causing her to miss some shifts at work and pay out of pocket for repairs. Without a bank account or good credit, she had to take a high-interest loan to fix the car and now struggles with those payments. She postpones going to the doctor for her own health issues due to cost, which eventually sends her to the ER in a crisis. Each of these problems amplifies the others. Her situation isn’t solely the result of individual decisions; it’s also the result of systems that exact higher tolls on her because of her poverty. In this way, poverty can indeed be a trap that is extremely difficult to break – not because the poor are lazy or spendthrift (in fact, many budget meticulously), but because the odds are stacked against them through these extra burdens.

It’s worth noting that not all of these dynamics are visible or understood by those who haven’t experienced poverty. Middle-class or wealthy individuals might wonder, “Why don’t you just move to a cheaper area, or shop at a discount store, or save up an emergency fund?” The reality is that the barriers the poor face are often invisible to others. Moving requires money for a security deposit and moving truck; reaching a cheaper store might require a car you don’t have; saving is nearly impossible if every spare dollar is eaten by late fees or high utility bills. What may look like “bad choices” from the outside are frequently constrained choices shaped by an environment of scarcity and extra costs. In short, systemic cost burdens absolutely make poverty self-reinforcing. Climbing the economic ladder is hard enough; climbing it while each rung breaks or cuts into your hands (and pockets) makes it even harder. Understanding this cycle is the first step toward breaking it.

Policy Solutions: Reducing the Hidden Tax on Poverty

If being poor is so expensive, what can be done about it? Traditional anti-poverty policy has often focused on income supports – for example, raising the minimum wage, providing tax credits or direct assistance, and improving access to education and jobs. Those remain vital, but our examination suggests that policymakers should also focus on reducing the hidden “taxes” and cost burdens that disproportionately hit the poor. In other words, not just give the poor more money, but also stop systems from unfairly taking so much of their money. Addressing these structural issues could immediately improve disposable income and stability for low-income families. Here are some key areas and ideas:

- Affordable Financial Services: Expand access to no- or low-cost banking for low-income households. This could include encouraging banks or credit unions to offer basic checking accounts with no minimum balance and minimal fees, or even exploring public banking options. One proposal that’s gained traction is postal banking, where local post offices could offer simple financial services (cash check, small loans) at low fees, providing a safe alternative to payday lenders and check-cashers. Stronger regulation of predatory lending is also essential: setting strict caps on interest rates for payday and auto-title loans (many states have started doing this) can prevent the worst exploitation. Additionally, cracking down on excessive overdraft fees or making transaction processing faster (so that paychecks clear more quickly) would help people avoid cascading fees. The goal is to integrate the poor into the financial mainstream on fair terms, so they aren’t penalized for being “unprofitable” customers.

- Housing and Utility Relief: Increase the supply of affordable housing through measures like tax credits for low-income housing development, zoning reforms, and support for community land trusts. More affordable housing in good condition would alleviate the rent burdens that trap so many families. Tenant protections can also help – for example, stronger anti-gouging regulations to ensure landlords can’t exploit lack of options by charging inordinate rents for substandard units. Expanding housing vouchers or subsidies can immediately reduce what poor families have to spend on rent, freeing up money for other needs. On the flip side, policies to help low-income families move to areas with lower poverty (like mobility vouchers or assistance with relocation costs) can get them out of high-exploitation neighborhoods. For utilities, programs that assist with weatherization of homes (insulation, efficient appliances) and subsidies for energy bills can reduce the “poverty premium” paid in electricity/gas costs. Some states have programs to forgive or discount utility bills for low-income households during harsh winters or summers – these can be bolstered to prevent poor families from paying disproportionately to keep the lights and heat on.

- Food Access Initiatives: To combat food deserts, governments and communities can incentivize grocery stores or farmer’s markets to open in underserved areas. This might involve grants, tax breaks, or public-private partnerships to establish supermarkets in urban and rural food deserts. Mobile markets and food co-ops are creative solutions that have worked in some regions – essentially bringing fresh produce via trucks or community-run stores to the heart of food deserts. Another approach is expanding support for programs like SNAP (food stamps) and WIC, and ensuring they can be used for online grocery delivery where physical access is a problem. Some cities have implemented “double bucks” programs where food assistance dollars are worth double at farmers’ markets, both aiding farmers and improving low-income diets. Education and nutrition programs can go hand in hand with improved access – but the key is making sure healthy food is the convenient, affordable option, not a distant luxury.

- Healthcare Coverage and Preventive Care: Filling the gaps in health insurance coverage is critical. States that haven’t expanded Medicaid (a program for low-income individuals) could do so, covering millions more poor adults. Even beyond insurance, community health clinics that offer free or sliding-scale services can provide accessible primary care in low-income neighborhoods, helping catch issues early. Policies to cap the price of crucial medications (like insulin) and to fund programs that assist patients with transportation to medical appointments can remove some barriers the poor face in getting care. Medical debt protection is another avenue: some states are looking at limiting aggressive medical debt collection or even buying up medical debt to forgive it. The overarching aim is to ensure that no one has to choose between going to the doctor and paying the rent, and that an illness doesn’t spiral into financial ruin. Preventive care must be made truly accessible – it’s both more humane and cheaper in the long run than paying for emergency interventions.

- Transportation and Mobility: Improving public transit in low-income areas can yield huge benefits. Investments in bus routes, subsidized transit passes, and last-mile connection services (like on-demand shuttles in areas buses don’t reach) can make it feasible to live without an expensive car. Some cities have experimented with reduced fare or free public transit for low-income residents. Another aspect is curbing predatory auto practices: enforcing usury limits on car loan interest, holding “Buy Here, Pay Here” dealers to higher standards, and making sure consumers have access to fair auto loans (perhaps through community development financial institutions) so that a necessary car purchase doesn’t become a financial albatross. Also, regulating car insurance to reduce or eliminate the use of credit scores could make insurance pricing fairer (a few states have already banned credit score usage in insurance). In the long run, better urban planning that brings affordable housing closer to job centers or expands transit networks will reduce the transportation tax on the poor.

Beyond these specific measures, a broader shift in perspective is needed. Policymakers should analyze new proposals through the lens of “Will this reduce or increase the extra costs borne by the poor?” For example, if fees or fines are introduced (say, for late payments or certain municipal services), consider how they disproportionately hurt those with less slack in their budgets. Conversely, seemingly small changes – like eliminating a fee, simplifying an application, or providing a small subsidy at a critical moment – can have outsized impacts for someone on the edge.

Reducing the hidden costs of poverty won’t eliminate poverty by itself, but it can ease the pressure and give people a fighting chance to use any additional income or opportunities to actually get ahead, rather than constantly falling behind. In essence, if we can stop punishing people for being poor, we remove some of the barriers that keep them poor. That, in combination with education, job creation, and fair wages, can make the American Dream a bit more attainable at the lower rungs of the ladder.

Poverty Penalties Beyond the U.S.: An International Perspective

The “poor pay more” phenomenon is not unique to the United States – it exists in various forms around the world – but its severity and specific dynamics can differ greatly by country depending on social policies and market structures. Comparing the U.S. situation to other countries can be illuminating. In many other advanced economies, some of the burdens we’ve discussed are blunted by strong social safety nets or regulations, whereas in developing countries, certain poverty penalties can be even more stark in different ways.

Other wealthy countries: In Western Europe, Canada, Japan, and similar nations, universal or near-universal healthcare means that low-income individuals do not face the same financial barriers to medical treatment as Americans do. A poor person in Canada can visit a doctor or hospital without fear of a ruinous bill; in the U.S., that fear is very real. This significant difference removes one major poverty penalty (healthcare costs) from the equation abroad – medical debt is virtually nonexistent in countries with universal healthcare. Similarly, many countries have more robust public transit and affordable housing programs, which can reduce two other key costs. For instance, a low-income worker in a European city might rely on extensive public transit networks at low cost, whereas their U.S. counterpart might struggle with car expenses. Public housing or rent subsidies tend to be more generous in parts of Europe as well, meaning fewer people spend 50%+ of their income on rent. Additionally, regulations often protect consumers in areas like credit and utilities. Some European countries strictly limit payday lending or cap interest rates at a reasonable level by law, effectively preventing the kind of debt traps common in the U.S. Utilities and broadband are sometimes heavily regulated or subsidized to ensure basic affordability, so you might see fewer cases of the poor paying higher per-unit costs for energy or phone service.

That said, even in these countries there is recognition of a “poverty premium.” In the U.K., for example, studies have shown that people on low incomes often pay more for certain services – a well-known estimate a few years ago put the U.K. “poverty premium” at around £490 per year on average. This comes from things like higher electricity tariffs for those using prepay meters (often the poor use prepay which charges higher rates), inability to get annual discounts by paying upfront (so the poor pay monthly and incur fees or higher rates), and higher insurance premiums in low-income postcodes. Insurance can be a hidden poverty tax even in Europe; for instance, if you can’t afford to pay a full year’s car insurance in one go, you pay monthly and insurers charge interest or fees on that (a practice some consumer advocates have labeled a “tax on being poor”). So while universal healthcare and other supports eliminate some burdens, other aspects – like credit costs, pricing structures, and market access – can still bite the poor. The difference is usually one of scale: the U.S. tends to have larger disparities because basic needs like healthcare, higher education, and housing involve more out-of-pocket costs here.

Developing countries: In low-income countries or emerging economies, the poverty penalty often takes on different forms related to infrastructure gaps. For example, in areas without clean tap water, the poor might have to buy water from vendors at much higher prices per liter than wealthier people who have piped water. In slums without electricity hookups, people pay more for alternative lighting (like kerosene lamps) than the electrified middle-class households pay for their power. Microcredit with high interest is sometimes the only source of loans for the poor in countries without inclusive banking. Additionally, the time cost of poverty is huge in many places: rural poor might walk hours to reach markets, or queue for an entire day to receive government rations or medical care, time that wealthier individuals don’t lose. These are all manifestations of the same principle: lacking money often forces you into costlier, less efficient ways of getting basic necessities.

One interesting comparison is how some countries have tried to actively tackle these poverty premiums. For instance, the concept of microfinance (small loans to poor entrepreneurs) arose to offer an alternative to exploitative local lenders; in some cases it’s been a success in empowering people, but in others it’s led to over-indebtedness. Some developing countries subsidize basic goods (fuel, food staples) to keep them affordable for the poor – which the U.S. generally does not do outside of specific programs like food stamps. In countries like India, direct efforts to bring banking to the poor (through mobile banking or postal banking) have parallels to what some propose in the U.S.

Overall, the comparison shows that the poverty penalty is a universal phenomenon – the poor often pay more in one way or another – but public policy can mitigate it significantly. The U.S. stands out among rich nations for how much is left to individuals to figure out and pay for on their own. That means the stakes of being poor are especially high in America. In contrast, in many other countries, collective solutions (be it healthcare, public transit, or social housing) reduce the degree to which individuals are punished financially for their poverty. Yet even in those places, vigilance is needed to ensure businesses or systems don’t sneak in extra charges for the poor. The ultimate goal, globally, would be to design systems that are fair – where basic human needs and services are accessible to all at a reasonable and equal cost. Studying how other countries reduce the “being poor is expensive” problem can offer valuable lessons for U.S. policymakers and vice versa.

Why Poverty Is So Expensive In America

The “poverty penalty” in America shines a harsh light on the everyday economics of inequality. It reveals that poverty is not just about insufficient income – it’s also about excess costs. A dollar in a poor person’s hand simply does not go as far as a dollar in a rich person’s hand, because so many tolls are extracted along the way. These tolls come in the form of higher prices for basic goods, exorbitant fees and interest for financial services, health costs from treatable issues gone unchecked, and lost time and opportunities due to unreliable transportation and infrastructure. Together, they form an invisible web that holds low-income individuals and families in place, even as they strive to move up.

Recognizing the poverty penalty is the first step toward addressing it. It challenges the notion that if people just worked harder or budgeted better, they would automatically escape poverty. Hard work and prudent budgeting are often already present; what’s missing is a fair playing field. No one should be punished for the “crime” of having no money by being charged more for life’s necessities. As a society, reducing these hidden taxes on the poor is a matter of justice as much as economics. It means re-examining policies and business practices that, intentionally or not, put extra burdens on those least able to bear them.

Ultimately, tackling the cost of being poor requires a mix of compassion, smart policy, and sometimes bold reforms. Whether it’s capping a predatory interest rate, opening a grocery store in a food desert, or expanding healthcare access, the solutions aim to remove hurdles rather than simply urging individuals to jump higher. If successful, such efforts won’t just save money for those who are struggling – they will also empower people to use their energy and resources toward progress (education, entrepreneurship, better jobs), instead of constantly paying off the past. Breaking the cycle of poverty is difficult, but reducing the poverty penalty is a tangible target. By making poverty less expensive, we can make it less persistent. In a country as wealthy as the United States, that is not only possible; it is imperative if the American ideal of equal opportunity is to mean something real for all its citizens.