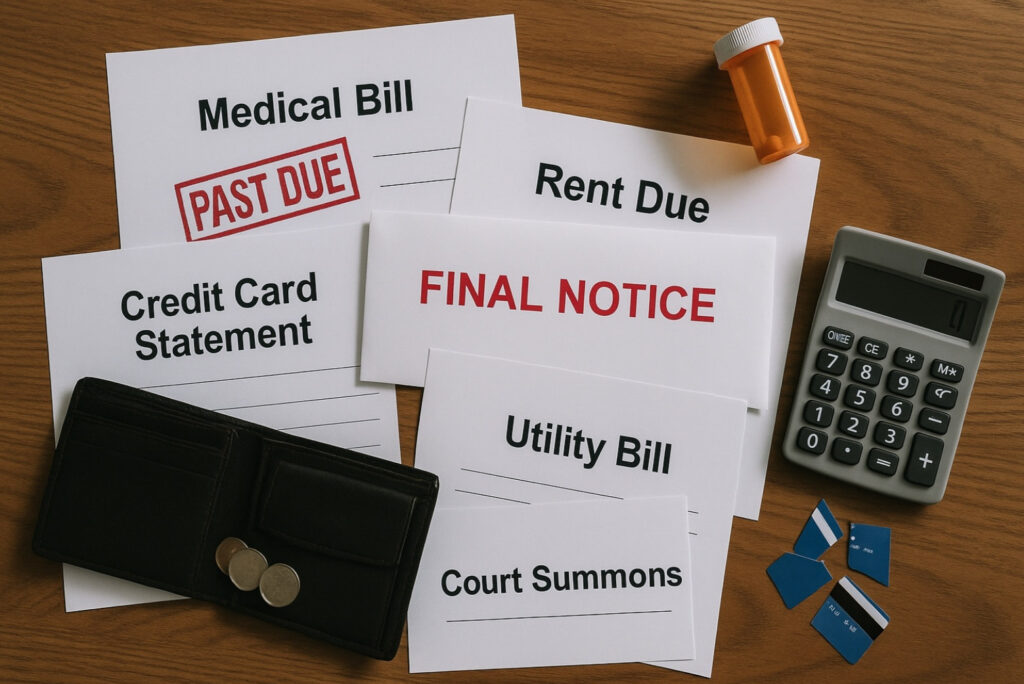

In the United States, personal bankruptcy is less a story of individual financial irresponsibility and more a predictable outcome of systemic fragility, where a single shock can trigger a devastating chain reaction. Overwhelmingly, the primary catalyst is a health crisis, saddling even the insured with crippling medical debt just as illness cuts their income, but this is powerfully compounded by job loss, unaffordable housing, and high-interest credit cards used as a desperate lifeline for necessities. These personal catastrophes unfold within a national framework of thin safety nets—tying healthcare to employment, offering limited unemployment benefits, and lacking price controls—which forces families to use high-risk credit to bridge the gap between stagnant wages and the soaring costs of basic living. Ultimately, bankruptcy serves as the nation’s brutal but necessary reset button, a judicial acknowledgement that for many, the American Dream has become a financial trap from which there is no other escape.

U.S. personal bankruptcy filings peaked dramatically in 2005 (over 2 million cases) and surged again around the Great Recession, before declining. In recent years, filings have begun rising once more, with over 517,000 bankruptcies in 2024 – a 14% jump from the prior year. Economists warn this uptick reflects mounting household pressures as pandemic aid fades, inflation soars, and debt loads become unsustainable. Behind each statistic is a personal financial collapse. This report investigates the leading causes pushing ordinary Americans into bankruptcy and the systemic failures turning personal misfortune into financial ruin.

Medical Debt: When Illness Leads to Insolvency

For hundreds of thousands of Americans each year, a medical diagnosis can mean financial devastation. In a nationwide survey of bankruptcy filers, 65% cited medical issues – either exorbitant bills or time lost from work due to illness – as a factor in their bankruptcy. In fact, an estimated two-thirds of U.S. personal bankruptcies are tied to medical debt or health crises. This makes health-related debt the single largest driver of personal bankruptcies in America, far outpacing other causes. By contrast, in countries with universal health coverage, medical bankruptcy is virtually nonexistent. The United States remains an outlier where a serious illness or injury can wipe out a family’s savings.

The reasons are not hard to find. Medical costs in the U.S. are astronomically high, and even having insurance is no guarantee of protection. Over 41% of U.S. adults currently carry some form of medical debt, whether on credit cards, payment plans, or personal loans. High deductibles, uncovered prescriptions, surprise out-of-network charges – all can leave patients with enormous bills. The Kaiser Family Foundation found that about 1 in 4 Americans with medical debt have considered bankruptcy as a way out. “I had insurance, but the deductible and denied treatments left me owing tens of thousands,” says one patient; stories like hers are strikingly common. Many are forced to choose between paying for lifesaving care or staying afloat on other bills.

Medical problems often create a double jeopardy: not only do bills pile up, but an illness or injury can cost someone their paycheck. A health crisis might mean weeks or months out of work, or even job loss entirely, especially for those without paid medical leave. In a cruel cycle, losing one’s job often means losing health insurance too – just as expensive treatment is needed. This one-two punch of lost income and high medical bills is a primary catalyst for bankruptcy. Even programs meant to help, like COBRA coverage, are prohibitively expensive when one is unemployed. The outcome is that medical bankruptcies occur at rates unparalleled in the developed world. Outside the U.S., it’s virtually unheard of to lose your home or life savings due to medical bills, but in America, sickness and injury frequently spiral into financial collapse.

Systemically, the U.S. healthcare structure leaves gaping holes in the safety net. The nation is unique among wealthy countries in lacking universal health coverage and in allowing health expenses to reach crushing heights. Insurance gaps and out-of-pocket costs are enormous contributors to personal insolvency. A 2015 study estimated medical bills contribute to one million U.S. bankruptcies annually. From chemotherapy medications priced at $15,000 a month to $250,000 emergency surgeries, even middle-class families can drown financially from a single serious diagnosis. Medical debt doesn’t just strain finances – it forces Americans to make agonizing trade-offs. Over one-third of people with medical bills report skipping basics like food, heating, or housing to pay those debts. Ultimately, the inability to pay for both health and home pushes many to seek bankruptcy as a desperately needed reset.

Job Loss and Income Shocks: The Precipice of Unemployment

A job is more than just a paycheck – it’s a lifeline keeping many households from the brink. It is no surprise, then, that loss of income is cited as the number one cause of personal bankruptcy in America. In the Consumer Bankruptcy Project’s surveys, a stunning 78% of filers pointed to a drop in income – often from a layoff, job termination, or significant pay cut – as a key reason they filed for bankruptcy. Similarly, earlier studies found that sudden income disruption was the most pervasive trigger for household bankruptcy, with about 70% of bankruptcy families with children reporting they filed after the primary breadwinner lost a job. Without steady wages, even a brief period of unemployment or underemployment can cascade into missed rent, defaulted loans, and mounting debt.

The backdrop to this grim statistic is an economy where millions live paycheck to paycheck, lacking any cushion for hard times. As of late 2023, roughly 78% of Americans were living paycheck to paycheck. For families on the financial edge, the loss of a job means bills immediately become unpayable. Most households have little to no emergency savings; many rely on each week’s pay to cover essentials. So when a layoff or reduction in hours hits, they are instantly at risk of falling behind on mortgages, car payments, and credit cards. Unemployment insurance, while helpful, replaces only a fraction of lost wages and is temporary. For those whose jobs also provided health insurance, losing employment can expose them to the full cost of medical care at the worst possible time. In this way, job loss and medical crises often intersect – a person gets sick and can’t work, loses income and insurance, then faces both medical bills and no paycheck. It’s a recipe for financial catastrophe.

Even short of outright job loss, any significant decline in income can tip a household into insolvency. Wage stagnation over decades has meant that incomes haven’t kept pace with the rising cost of living, leaving workers more vulnerable to shocks. Many Americans cobble together two or three jobs to stay afloat; if one gig ends or overtime is cut, the shortfall can be disastrous. The problem is especially acute in an era of at-will employment and minimal labor protections. The United States notably remains the only wealthy nation with no guarantee of paid sick leave for workers. This means millions risk losing wages or their job entirely if they fall ill or need to care for a family member. A single bout of flu or a minor injury can thus start an avalanche: lost income leads to missed bill payments, late fees, maxed-out credit cards, and eventually the need for bankruptcy protection. In short, when steady employment is so closely tied to basic security – from health insurance to housing – a break in that employment can unravel a household’s finances with alarming speed.

Credit Card Debt and Overspending: Plastic Path to Bankruptcy

America’s reliance on credit is a double-edged sword: it can smooth over short-term needs, but it often fuels a long-term debt spiral. Credit card debt – whether from overspending or just trying to cover basic expenses – is a leading contributor to bankruptcies. Surveys of bankruptcy filers indicate that roughly one-quarter cite credit card overuse or other forms of overspending as a major factor in their financial downfall. Mountains of high-interest debt can accumulate quickly when people live beyond their means or when they lean on credit to cope with emergencies. What begins as a few thousand dollars on a card for “temporary” expenses can snowball with compound interest into an unpayable burden. The average U.S. household carrying credit card balances now owes over $21,000 in credit card debt – a staggering figure that helps explain why so many eventually seek relief in bankruptcy court.

The scale of America’s credit card problem is unprecedented. U.S. consumers’ collective credit card debt hit a record $1.17 trillion in late 2024. To put that in perspective, credit card balances have surged by nearly 50% since 2021, as families increasingly turned to plastic to cope with pandemic disruptions and, more recently, with inflation’s squeeze on budgets. Credit cards often become the de facto safety net when wages lag behind the cost of living. But using credit to pay for groceries, utility bills, or medical co-pays means taking on debt for everyday life – debt that comes with interest rates now averaging a punishing 20–30%. In 2023 and 2024, as interest rates rose across the economy, many credit card APRs climbed to record highs (averaging about 28.6% by late 2024). For indebted households, that means finance charges piling up faster than they can make progress on balances. Minimum payment requirements also increased, straining budgets further. It’s no surprise that the share of Americans making only minimum payments hit an all-time high of 10.75% – a sign of people barely treading water.

Credit card debt often intertwines with other issues, serving as both symptom and cause of financial distress. A family dealing with a job loss or medical bills might turn to cards to stay afloat – which temporarily masks the pain but ultimately deepens the debt hole. Others fall into the trap of “buy now, pay later” consumption, spending beyond their means due to easy credit availability and then struggling to service the debt. High interest ensures that what started as a manageable sum can double or triple if only minimums are paid. Many bankruptcy narratives include a moment of realization when credit obligations become mathematically impossible to clear. By then, late fees and over-limit penalties may be accruing, credit scores plummet, and creditors start calling daily. In the end, personal bankruptcy becomes the only way out of a credit card quagmire that might have been years in the making. As one counselor noted, “High-interest credit is a trap – once you’re in deep, it’s nearly impossible to climb back out without drastic measures.”

Unaffordable Housing: Homes Lost to Debt and Foreclosure

Owning a home has long been part of the American Dream, but for many it has turned into a nightmare of debt. Mortgages and housing costs are now the single largest component of household debt in the United States, accounting for about 72% of all consumer debt. When those mortgage payments become unmanageable, bankruptcy often follows. Housing-related financial strain typically emerges in two ways: either homeowners take on mortgages beyond what they can afford (sometimes encouraged by lenders), or an external shock (job loss, divorce, rising rates) suddenly makes an affordable loan unaffordable. In both scenarios, people risk falling behind on payments and ultimately foreclosure on their homes. To prevent or delay foreclosure, many turn to Chapter 13 bankruptcy, which can restructure mortgage arrears, or Chapter 7, which might wipe out other debts and free up income for housing. Roughly 1 in 5 bankruptcies in some analyses involve a serious housing credit issue, such as a foreclosure or eviction proceeding. Indeed, one study noted that about half of households filing for bankruptcy were doing so on the heels of some legal action against their property – a foreclosure notice, a car repossession, or wage garnishment. Housing problems are both a cause and a consequence of bankruptcy.

In boom times, many Americans stretched to buy homes with slim financial margins for error. For years before the 2008 crash, lenders approved buyers for mortgages larger than they realistically could manage, assuming home values would keep rising. When the housing bubble burst, foreclosures spiked and personal bankruptcies surged in tandem as millions were left with homes worth less than their loans and payments they could no longer meet. While that specific crisis has passed, housing affordability remains a severe challenge. Home prices and rents have climbed to record highs in many regions, outpacing wage growth. “Unaffordable housing” has become a term to describe the reality for a growing segment of the population that devotes well over 30-40% of income to shelter. All it takes is a slight uptick in interest rates on an adjustable mortgage, a missed paycheck, or an unexpected expense, and a household can fall behind. In 2023–2024, interest rate hikes did exactly that to variable-rate mortgage holders – sending some monthly payments hundreds of dollars higher. For those already on the edge, the increase proved ruinous. Older Americans, too, face housing-cost pressures, with many carrying mortgage or home-equity debt into retirement on fixed incomes.

Bankruptcy provides a last-resort option to deal with housing debt. Chapter 13 bankruptcy, for instance, can halt a foreclosure and allow a homeowner to catch up on missed payments over time. But saving the home is not always possible; some must surrender their house in bankruptcy and walk away from their largest asset. Renters are not immune either – falling behind on rent can lead to evictions, and some end up in bankruptcy court to discharge the back rent and other debts. Behind the statistics are human stories: a lost job or medical emergency leads to missed mortgage payments; a spike in rent forces reliance on credit cards for basics, which then snowball. These scenarios demonstrate how tightly housing security is linked to overall financial health. When housing becomes unaffordable, bankruptcy can become the final refuge for those trying to escape the crush of shelter-related debt.

Student Loans: The Education Debt Trap

For decades, Americans have been told that a college education is the ticket to a better future. But for many, the cost of that ticket – student loan debt – has itself become a trap leading toward financial ruin. Student loan burdens are rarely dischargeable in bankruptcy, yet they still play a significant role in many bankruptcy cases. About one-quarter of bankruptcy filers carry student loan debt. These loans often cannot be wiped out except in extreme circumstances, but their presence can push borrowers into default on other debts and expenses. Consider a graduate carrying a $600 monthly student loan payment on a modest salary: if they also face credit card debt, a car payment, and rent, their budget leaves no room for error. Any shock – a layoff, medical bill, or even a broken car – can make their debt load unsustainable. Many end up filing bankruptcy to discharge what debts they can (credit cards, medical bills, personal loans) in order to free up enough income to keep paying the student loans. In essence, bankruptcy becomes a tool to manage the crushing weight of education debt indirectly, since the loans themselves are anchored to the borrower for life in most cases.

Recent policy changes have offered a faint glimmer of hope on this front. In 2022, new guidance was introduced to make discharging federal student loans in bankruptcy slightly easier for those in dire straits. Through an “adversary proceeding,” borrowers can seek to prove that repaying the loans would impose an undue hardship – a notoriously high bar. Early results show promise: by 2024, 98% of borrowers who pursued bankruptcy under the new rules succeeded in getting their student loans discharged or reduced. While this affects only a small number of people (given the difficulty and rarity of even attempting it), it signals acknowledgment that student debt can indeed be a life-long albatross. The vast majority of student borrowers, however, remain on the hook. Many young Americans begin their working lives tens of thousands of dollars in debt. If a good-paying job materializes, they might manage; if not, they could teeter on insolvency. Notably, researchers have found that about 40% of borrowers who filed for bankruptcy with student loans never actually obtained a degree. These individuals incurred debt but didn’t see the income boost that a diploma might have provided, leaving them in a particularly harsh bind.

The nexus between student loans and bankruptcy is also evident in broader economic trends. The explosion of college costs (far outpacing inflation) and the corresponding rise in student borrowing – now over $1.7 trillion nationally – means many households juggle education debt alongside mortgages, car loans, and everyday expenses. Young adults put off buying homes, starting businesses, or even having children because of their debt obligations. And if they fall behind, lenders can be relentless – student debt delinquency can lead to wage garnishments and seized tax refunds, further destabilizing finances. Bankruptcy court doesn’t easily relieve student borrowers, but it can shield them from other creditors and legal actions while they regroup. In sum, student loans may not always show up as “discharged” in bankruptcy statistics, but they form part of the debt mosaic that pushes people to the breaking point. As one analyst noted, “Student debt is the elephant in the room – you can’t bankrupt it away easily, yet it’s bankrupting the future of many young Americans.”

Legal and Divorce Expenses: When Justice and Tragedy Come at a Cost

Personal bankruptcy often has a deeply human story behind it, and frequently it’s a story of personal crisis. Divorce is one such crisis that, beyond emotional turmoil, brings profound financial fallout. In fact, divorce and related legal costs are among the top causes of bankruptcy filings. Approximately 1 in 10 bankruptcies stem from divorce or separation. When a marriage falls apart, so do economies of scale: suddenly one household splits into two, doubling living expenses while the total income stays the same or even drops. Legal fees for divorce proceedings, custody battles, or alimony disputes can easily run into the tens of thousands of dollars, draining savings accounts and retirement funds. Bank accounts get divided, assets are sold or fought over, and both partners may emerge in worse financial shape. It is not uncommon for recently divorced individuals to find themselves unable to keep up with mortgage payments or joint debts they once managed with a spouse’s help. Many end up in bankruptcy simply to gain relief from debts that became unpayable after the split.

Legal expenses beyond divorce can also drive people to insolvency. Fighting a lawsuit, for instance, can bankrupt even middle-income individuals if they lack adequate insurance or resources. Consider someone who is sued after a car accident or for a business dispute: attorney fees, court costs, and potential judgments can climb astronomically. Without rich savings or umbrella insurance policies, an unfavorable verdict might force bankruptcy as the only way to handle the liability. Even winning in court can be financially devastating if legal fees outstrip one’s ability to pay. Another scenario involves criminal legal fees – a person accused of a crime (or a family member of someone accused) might spend every last dollar on defense costs. If acquitted, they could still be buried in debt; if not, the combination of legal bills and loss of income (due to incarceration or reputation damage) can be ruinous. In all these instances, bankruptcy provides a legal shield to discharge debts and stop collections. It can erase credit card balances used to pay lawyers, forgive unsecured loans taken out to fund legal battles, and stay any further wage garnishments or asset seizures ordered by courts.

Beyond formal legal proceedings, there are also the “soft” legal-related costs that push people to the brink – like the fees associated with probate and settling an estate after a family death, or the costs of an adoption or custody fight. Such life events often come with price tags people don’t anticipate. A death in the family, for example, may leave survivors with funeral expenses and lingering debts of the deceased. If the estate can’t cover them, surviving relatives sometimes shoulder those bills and quickly find themselves underwater financially. Bankruptcy in those cases can serve as a painful but necessary clean slate. Taken together, these legal and family-related causes underscore that bankruptcy is frequently triggered by life’s most stressful transitions. No one plans for a costly divorce or a lawsuit, but when they hit, the financial damage can be irreparable without the drastic remedy of bankruptcy. As counselors note, it’s not that people go bankrupt from a single lawyer’s bill; it’s that the cascade of costs and lost income around these events becomes overwhelming. Bankruptcy is the emergency exit when the usual avenues of juggling and negotiating debts have closed.

Inflation and the Rising Cost of Living: The New Bankruptcy Wildcard

While classic causes like medical bills and job loss have long been linked to personal bankruptcies, a newer factor looms large today: inflation. Over the past two years, Americans have been squeezed by the highest inflation rates in four decades. Prices for essentials – food, housing, utilities, gas – have skyrocketed, eroding the purchasing power of paychecks. When the cost of living climbs faster than incomes, many households respond by taking on more debt to cover the gap. They swipe credit cards to pay for groceries, or they fall behind on bills and incur late fees. Slowly, a debt snowball forms. Inflation also pushes up interest rates (a strategy by the Federal Reserve to cool the economy), which in turn makes existing debt more expensive to service. By 2024, interest rates on mortgages, credit cards, and personal loans had all risen substantially, adding to monthly payment burdens for millions of borrowers. According to the American Bankruptcy Institute, these twin forces – high prices and high borrowing costs – have been “expanding debt loads” for households and contributing to the recent rise in bankruptcy filings.

Consider a typical family budget: if rent increases by $200 a month, the grocery bill by $100, and the gas tank costs $50 more to fill, that family might see an extra $350 (or more) in monthly expenses compared to a year prior. Unless their income rose equivalently, that shortfall has to be covered somehow. Some dip into savings (if they have any), but with 78% living paycheck to paycheck, most have little cushion. Others cut back on discretionary spending, but there’s only so much to trim when inflation hits staples. Inevitably, many resort to credit – running up balances or taking out small loans. Fast forward a year or two of high inflation, and these families are now saddled with debts they never would have incurred had prices stayed stable. When interest accrues and minimum payments mount, it’s a slow grind into insolvency. We are now seeing the fallout: bankruptcy attorneys across the country report more clients citing general cost-of-living increases as the final straw that broke their finances.

Inflation also indirectly exacerbates other bankruptcy triggers. It can fuel higher medical charges (hospital systems raise prices to keep up with costs), steeper tuition (pushing more student borrowing), and demands for wage increases that, if unmet, effectively translate to wage cuts in real terms. For those on fixed incomes, like many retirees, inflation is especially pernicious – if Social Security or pensions don’t adjust sufficiently, seniors may accumulate debt just to maintain a basic standard of living. Indeed, the fastest-growing demographic of bankruptcy filers in recent years has been Americans over 65, a cohort heavily impacted by medical costs and living expenses on fixed income. Inflation can be the silent thief of financial security, and when paired with America’s thin social safety nets, it becomes a direct pipeline to the bankruptcy courts. The recent surge in filings (up nearly 17% in 2023 and climbing further in 2024) has been linked by experts to these inflationary pressures and the end of temporary COVID-era relief measures. In short, while few people list “inflation” on their bankruptcy paperwork as a cause, it lurks behind many of the debts and defaults that ultimately drive them to seek legal relief.

A Broken System: Policy Gaps and the Perfect Storm of Debt

Each of the causes of bankruptcy – medical crises, job loss, credit debt, housing woes, student loans, legal battles, and inflation – is a personal catastrophe. But amplifying all of them is a broader systemic problem: an American safety net full of holes. The United States’ policy landscape often leaves individuals to fend for themselves in the face of life’s risks. Consider healthcare: the U.S. is the only wealthy nation without universal health coverage, and it spends more per capita on healthcare than any peer nation. Yet that spending hasn’t prevented tens of millions from incurring medical debt. Insurance tied to employment means that a health crisis can be financially ruinous especially if it also costs someone their job. Meanwhile, other countries long ago decided that citizens shouldn’t mortgage their futures for medical treatment; as a result, medical bankruptcy abroad is a rarity. Here, it’s a commonplace tragedy.

The labor system is another linchpin. With weak protections for workers, Americans face job loss and income drops with little support. Unemployment benefits in the U.S. replace only a fraction of wages and expire quickly, often well before a new job is found. And unlike nearly all advanced economies, the U.S. has no federal guarantee of paid sick leave or paid family leave. That means a significant illness or caregiving need often forces people out of work or cuts their income, as discussed earlier. When life happens – a child falls ill, an aging parent needs help, an expectant mother has complications – there is no system-wide backstop to keep that worker’s income steady. In practice, many end up borrowing to get through the crisis, or they simply fall behind on bills, setting the stage for bankruptcy. Wage stagnation over decades has further eroded Americans’ ability to absorb shocks. Productivity and the cost of living have risen, but median wages in real terms have barely budged for large swaths of workers. The result is a reliance on credit to fill the gap between income and expenses. Household debt (mortgages, credit cards, autos, student loans) has ballooned to over $17 trillion nationwide, a figure that reflects not just consumer choices but structural necessities for many.

Another systemic contributor is the easy availability of high-interest credit paired with minimal financial education. From a young age, Americans are bombarded with credit card offers and loan opportunities, yet personal finance is rarely a required subject in school. This over-reliance on credit as a financial buffer is essentially a privatized safety net – instead of strong social programs, people are left to rely on Visa and Mastercard in emergencies. It works, until it doesn’t. Payday lenders and subprime credit purveyors often prey on those already in precarious positions, leading to debt traps that are nearly impossible to escape without legal intervention. The bankruptcy system itself, while providing relief, was made more onerous by a 2005 law (BAPCPA) that added paperwork and costs for filers. Though intended to curb abuse, it mostly served to make the process more complex for genuine hardship cases. Even so, the relentless rise in filings during tough economic times underscores how deeply people need that lifeline when all else fails. During the Great Recession and the early pandemic, filings soared in tandem with layoffs and lost insurance coverage. When government relief programs kicked in (stimulus checks, eviction moratoriums, expanded jobless benefits), bankruptcies temporarily ebbed – proof that policy can make a difference.

In the absence of robust social safety nets, personal bankruptcy has become a catch-all last resort. It is effectively part of the American social contract: there may be little help to prevent you from falling into crisis, but there is a legal process to wipe the slate clean after the fall. This process, however, comes with its own costs – emotional stigma, damaged credit for years, and not everyone qualifies for full relief (some debts like student loans or recent tax bills often stick around). The prevalence of bankruptcy in the U.S. is a symptom of deeper failures – in healthcare affordability, in worker protections, in income inequality, in consumer finance regulation. Each bankrupt family is a story of personal hardship compounded by systemic shortcomings. Policymakers and experts increasingly view the high rate of bankruptcies as a sign that the “personal responsibility” narrative is overly simplistic: yes, mismanagement can lead to bankruptcy, but far more often, it’s bad luck and a weak safety net that push financially responsible people over the edge. As the head of a bankruptcy institute noted, rising filings signal mounting economic challenges as debt loads expand and prices soar, and that bankruptcy remains a “safe haven” for distressed consumers in the face of these headwinds.

Who Declares Bankruptcy? A Snapshot of Age, Income, and Family Factors

Bankruptcy can strike anyone, but not all Americans face equal risk. Data on who files for bankruptcy reveals patterns that underscore economic disparities. Below is a breakdown illustrating how different age groups, income levels, and family structures experience bankruptcy:

| Demographic Group | Share of Bankruptcy Filers |

|---|---|

| Age 30–49 | ≈58% of filers (prime working age adults bear the brunt) |

| Age 65 and older | 18.7% of filers by 2022, up from 4.5% in 2001 (fastest-growing group) |

| Median age | 49 years old (half of filers are middle-aged or older) |

| Low-income households | ≈85% had income below the 40th percentile (median income of filers is far below the national median) |

| Single women | ~33% of filers (largest single demographic; many are single mothers) |

| Single men | ~15% of filers |

| Married/partners | ~52% of filers (often filing jointly as a household) |

| Education debt | 25% of filers hold student loan debt (even if student loans aren’t discharged, they factor into insolvency) |

These figures paint a picture of who is most vulnerable. Middle-aged Americans are in the eye of the storm – juggling mortgages, raising children, and often supporting aging parents, all while having modest savings. It is telling that those in their 30s and 40s dominate filings; this is the life stage of highest expenses. At the same time, the surge in older filers highlights that even retirement-age Americans are not immune – many carry debt into retirement or face medical bills that overwhelm fixed incomes. On the income side, bankruptcy is largely a middle and lower-income phenomenon. Households below the median income (often well above the poverty line but struggling with debt) form the bulk of filers. Wealthier Americans rarely file bankruptcy individually (though they may have business bankruptcies) because they have more buffers and assets to maneuver. It’s the economically vulnerable – those living on the edge of solvency – who are one economic shock away from ruin.

Family structure also plays a role. Single-parent households, especially those led by women, appear frequently in bankruptcy records. A single mother with children, for example, has one income to cover a range of expenses that dual-income couples share, making her finances precarious. The data showing one-third of filers are single women, compared to 15% single men, likely reflects the added burdens many women carry, including wage gaps and caregiving responsibilities. Married couples comprise about half of filers, which often means they are filing jointly after a shared crisis (like a failed business, medical event, or job loss affecting one or both). It’s important to note that bankruptcy does not discriminate – men and women file in roughly equal total numbers, and people of all ages from young adulthood to senior years can end up in court. But the propensity is higher in certain groups due to the economic inequalities baked into society. Lack of a college degree, for instance, is more common among filers than the general population, reflecting how education (or lack thereof) correlates with financial stability. Ironically, those with some college but no degree are in a worst spot – often carrying student debt but without the higher earnings a diploma might have provided.

The snapshot above underscores that personal bankruptcy is often less about personal failings and more about personal circumstances meeting structural vulnerabilities. It’s frequently said that a majority of Americans would struggle to afford a $1,000 emergency – bankruptcy filers are those for whom the emergency came, and was far costlier than $1,000. They are our neighbors, coworkers, and family members, navigating a financial system that offers plenty of ways to fall into debt and far fewer ways to climb out without lasting damage. Each statistic in the table represents thousands of lives upended – and a societal challenge that remains urgent and pervasive.

The Cost of Bankruptcy and the Urgency for Change

Personal bankruptcy in America sits at the intersection of individual misfortune and systemic failure. Each case is a story of hardship – a cancer diagnosis, a factory shutdown, a marriage torn apart, a predatory loan – but collectively, they form a stark indictment of the status quo. Over half a million Americans now file for bankruptcy each year, seeking relief from debts that have become impossible to bear. These aren’t people looking for a free pass; most arrive at bankruptcy court as a last resort, often ashamed and defeated. As the data shows, the vast majority tried everything else first – cutting expenses, negotiating with creditors, borrowing from family – before the crushing weight of debt and circumstance left them no choice. In the words of one financial counselor, “They’re doing everything right and still falling short”. That so many hardworking, responsible people end up bankrupt speaks volumes about the landscape of risk in America today.

What will it take to reduce the tide of bankruptcies? The answers are as multifaceted as the causes. Tackling the medical debt crisis might involve comprehensive healthcare reform so that an accident or illness isn’t financially fatal. Preventing job-loss bankruptcies could mean strengthening unemployment insurance, mandating paid sick leave, or retraining programs that get people back to work faster. Reining in credit card bankruptcies might require tighter regulation of lending and interest rates – indeed, there are calls to cap credit card APRs that currently hover near 30%. Making higher education affordable (or student debt dischargeable) would alleviate one huge source of pressure on young families. Expanding affordable housing and assisting those in temporary trouble with mortgages or rent could stop the foreclosure-to-bankruptcy pipeline. And overarching all this is the need for a sturdier safety net – one that catches Americans before they plummet into a debt abyss, rather than expecting bankruptcy courts to mop up the aftermath.

For now, bankruptcy remains a bittersweet salvation. It does offer relief – debts wiped clean, collection calls silenced, a chance to rebuild from nothing – and for many it’s the fresh start that our bankruptcy laws intended it to be. But that fresh start comes at a high cost: ruined credit, stigma, and the trauma of financial collapse. In the world’s wealthiest country, it’s worth asking why so many of its citizens must resort to legal forgiveness to survive economic blows that citizens of other countries are shielded from. The stories and statistics in this investigation point to an uncomfortable truth: personal bankruptcy in America is less a reflection of personal irresponsibility and more a mirror held up to a society that allows medical emergencies, layoffs, and simple bad luck to destroy lives. Until the root causes – from sky-high medical bills to wage stagnation – are addressed, the bankruptcy courts will continue to fill with people whose only crime was to fall on hard times without a net. And as a society, we will continue to pay the price of those broken dreams and bankrupted futures.